Nelson Capital Management

The Fed Battles Inflation

Asset Management, Fixed Income, Investment Themes, Quarterly Commentary, The Economy

April 7, 2022

The Fed Battles Inflation

Since the pandemic market low on March 23, 2020, the equity market has at times seemed unstoppable. The S&P 500 rebounded to finish 18% higher in 2020, then rose another 28% in 2021. However, the first three months of 2022 have ushered in volatility and a cloudier market outlook. Even before Russia invaded Ukraine in the early morning hours of February 24, the S&P 500 had suffered a correction, falling more than 10% from its record high set on January 3rd. The tech-heavy Nasdaq index fell even more, down more than 20% from its high, officially entering bear market territory. The markets recovered much of their declines in the last few weeks of March, with the S&P 500 finishing the quarter down 4.85% and the Nasdaq down 9.5% from the start of the year.

Although the conflict in Ukraine has dominated the headlines, the primary culprits driving the market choppiness are inflation and the Fed’s plan to confront it. As the world has reopened and consumers have resumed normal activity, inflation numbers have run much higher than the Fed’s 2% target. The latest Consumer Price Index (CPI) report saw inflation hit 7.9%, the highest level in about four decades. After spending much of 2021 asserting that high inflation would be “transitory,” the Fed finally scrapped that word from its vocabulary in November of 2021.

..as inflation numbers have ticked higher, the Fed acknowledged that it would have to implement more restrictive monetary policy in order to get high inflation under control.

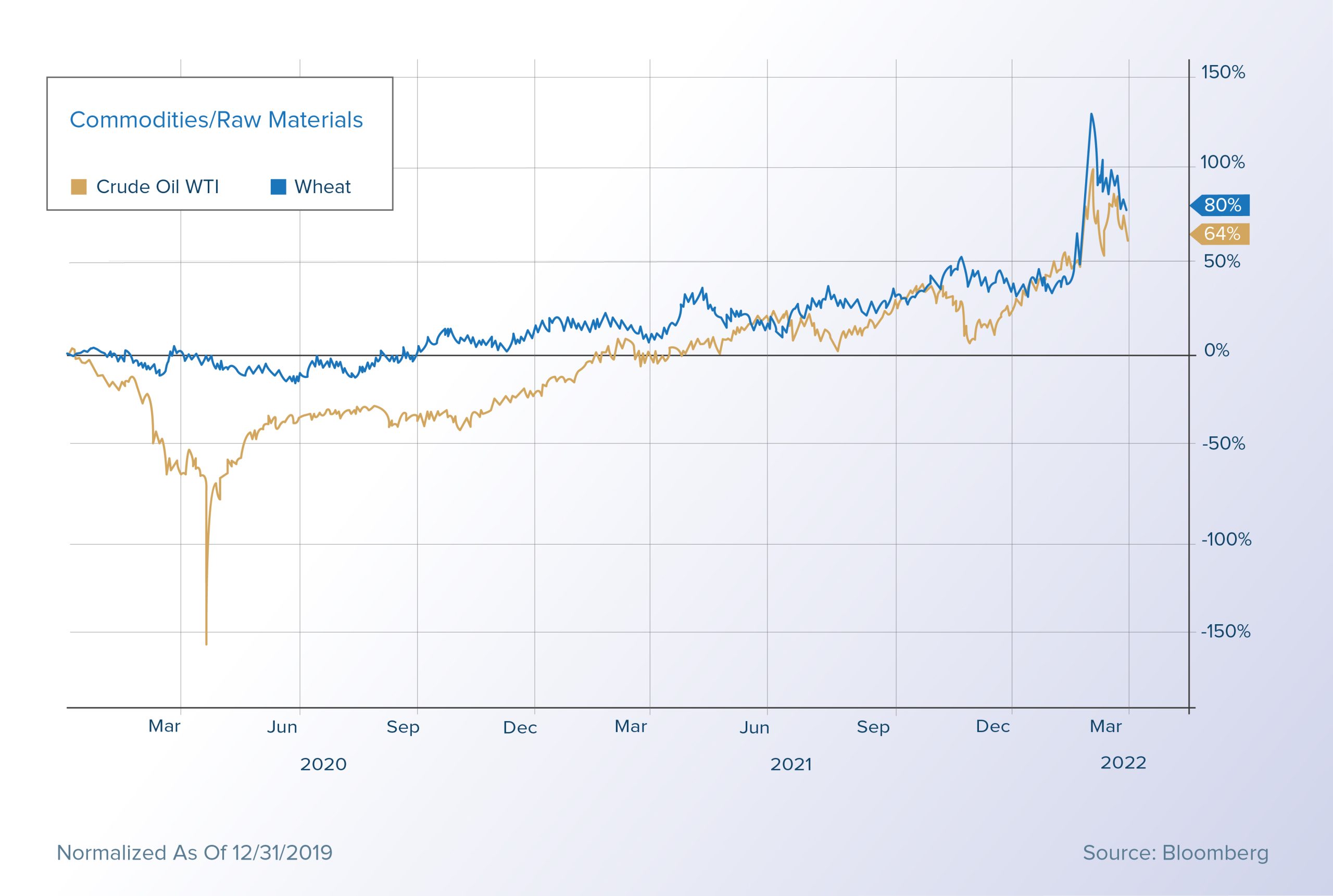

Supply chain problems have not only persisted, but have worsened amidst the intensifying war between Russia and Ukraine. Western sanctions on Russia, including a ban on Russian energy imports, caused prices of crude oil and natural gas to jump by more than 30%. Prices of wheat, corn, soybeans and fertilizer also soared as Ukraine and Russia are both major exporters of agricultural products. US consumers are feeling the pain of these higher prices at the grocery store and gas pump.

Supply chain problems have not only persisted, but have worsened amidst the intensifying war between Russia and Ukraine. Western sanctions on Russia, including a ban on Russian energy imports, caused prices of crude oil and natural gas to jump by more than 30%. Prices of wheat, corn, soybeans and fertilizer also soared as Ukraine and Russia are both major exporters of agricultural products. US consumers are feeling the pain of these higher prices at the grocery store and gas pump.

In the wake of the pandemic, the Fed advocated an expansionary monetary policy, in order to stimulate growth that had been decimated by Covid-19. For much of last year, the Fed indicated that it would not raise its benchmark interest rate aggressively, nor would it rush to shrink the size of its balance sheet, which had doubled to $8 trillion since the start of 2020. However, as inflation numbers have ticked higher, the Fed acknowledged that it would have to implement more restrictive monetary policy in order to get high inflation under control. Fed Chair Jerome Powell recently commented that the Fed would need to move “expeditiously” to return monetary policy to a more neutral level, and that the Fed may eventually need to go to a more restrictive level if needed to restore price stability. The Fed implemented its first post-pandemic rate hike at its March meeting, increasing its target rate by 0.25%, and projected six more rate hikes in 2022, followed by four rate hikes in 2023. This would indicate the Fed Funds Target Rate is set to reach about 2.75% by the end of 2023.

Although the Fed has only initiated one single 0.25% increase in its target rate, the specter of higher interest rates spooked the equity market. Higher interest rates translate to a higher cost of capital, a particularly painful prospect for high-flying growth companies that have become dependent on access to very cheap money. So far this year, the majority of the pain in the equity market has been felt by unprofitable technology companies. In a higher interest rate environment, these companies will either need to tighten their belts and start generating cash flow or pay up for more capital. Nevertheless, equity valuations have come down across the board. The forward price-to-earnings ratio of the S&P 500 (using forward-looking analyst estimates for expected future earnings) has dropped to about 20x from about 23x at the start of the year. This valuation is still above the 25-year average of about 17x.

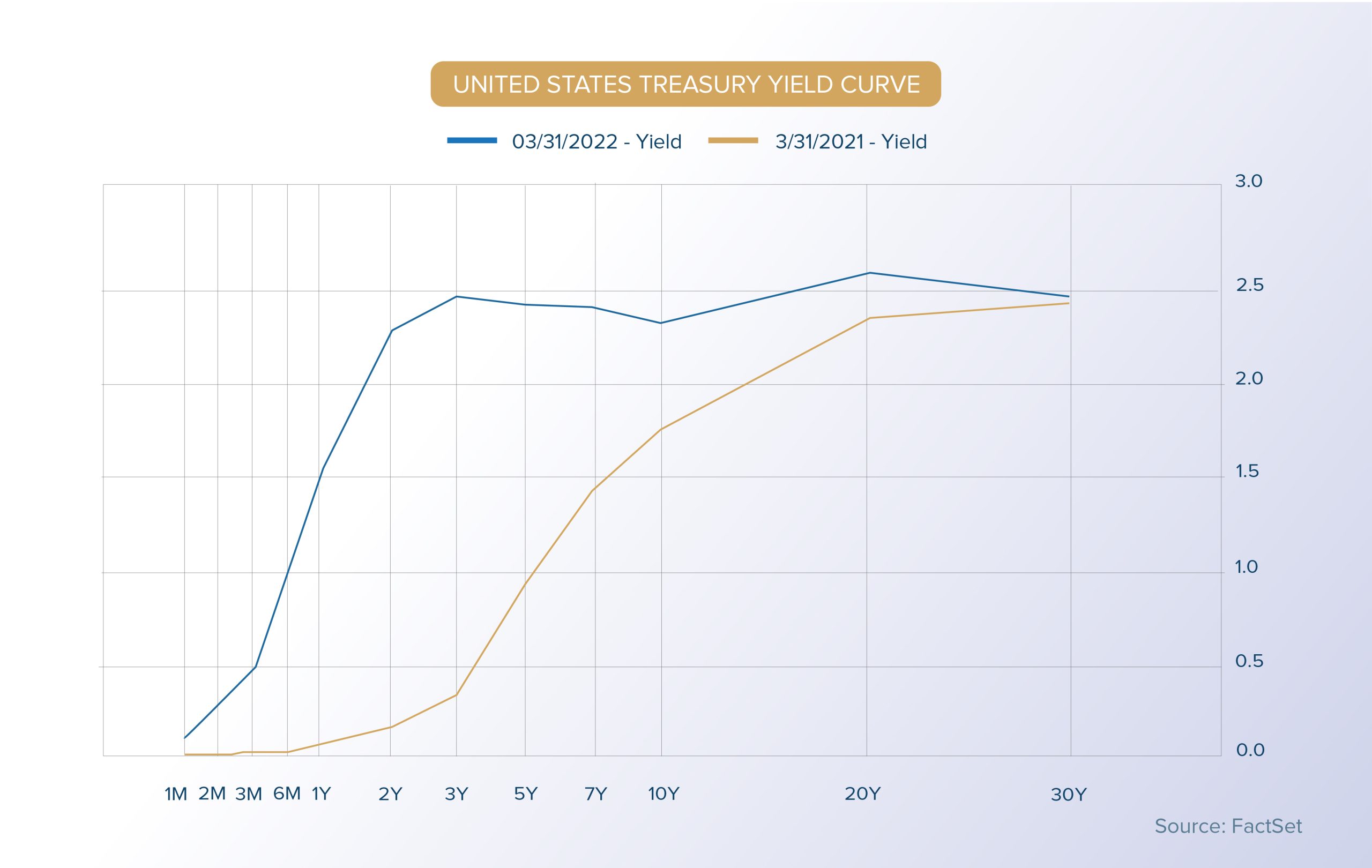

The bond market’s reaction to the Fed’s pivot has been equally dramatic. The yield on the 10-year US Treasury has risen nearly 100 basis points, from 1.50% at the start of the year to just under 2.50%. Short-term rates have risen even more, with the yield on the 2-year US Treasury up over 150 basis points from 0.75% to 2.28%. The bond market believes that the Fed will frontload its rate hikes to rein in runaway inflation.

Consumers are feeling higher costs from inflation, but are generally still in good shape. The labor market remains very tight, with job openings at around 11 million, compared to about 7 million pre-pandemic. This tight job market is putting upward pressure on wages, adding yet another inflationary factor, but also helping line consumer pockets and drive higher spending power. Companies continue to face rising costs of raw materials and labor, but have thus far been able to pass along these costs in the form of price increases. We are focused on companies with lower valuations and strong pricing power that offer goods and services consumers cannot do without. We believe these types of equity investments can perform well, even in a high inflation environment.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Capital Management, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

Receive our next post in your inbox.