Nelson Capital Management

A Tale of Two Markets

Investment Themes, The Economy

July 5, 2023

A Tale of Two Markets

“It was the best of times, it was the worst of times…”

During the second quarter of 2023, the equity market rallied nearly 9%. Fears surrounding the mid-March banking crisis seemed to dissolve, replaced by excitement over new artificial intelligence technology prospects. The S&P 500 entered a new bull market, finishing the quarter up over 20% since its low on October 14 of last year. The rally in the stock market has been primarily driven by seven large companies: Amazon, Apple, Alphabet, Microsoft, Nvidia, Tesla and Meta, with the latter three companies up over 100% since the start of the year. In fact, if we were to take an equal-weighted basket of these seven stocks, the year-to-date total return would be calculated at more than 86%. Meanwhile, an equal-weighted basket of the entire S&P 500 has returned only 5% in the same time period. Nevertheless, we have seen a recent uptick in fund flows into the equity market as the fear of missing out (FOMO) has set in.

The equity market seems to be brushing off recession concerns, taking a “glass half full” view of the economy. Headline inflation has declined more quickly than anticipated, to just over 4% in May from a peak of 8.5% a year ago. The Federal Reserve paused its interest rate hike campaign at its latest meeting in June, offering a respite, particularly to the beleaguered banks, after over a year of aggressive rate increases. The labor market has begun to loosen but is still relatively strong with low unemployment and jobless claims, elevated job openings numbers, and a solid track record of jobs added in the last several months. Consumer spending remains healthy, particularly on services such as entertainment, travel, and leisure. Company earnings thus far have been better than feared, with earnings per share (EPS) down less than 1% compared to analyst estimates for a ~6% decline. Volatility has been low, with the VIX “fear index” reaching a three-year low. The equity market appears to buy the argument that the US is headed for a “soft landing” scenario, in which inflation comes down and a recession is avoided.

The equity market seems to be brushing off recession concerns, taking a “glass half full” view of the economy. Headline inflation has declined more quickly than anticipated, to just over 4% in May from a peak of 8.5% a year ago. The Federal Reserve paused its interest rate hike campaign at its latest meeting in June, offering a respite, particularly to the beleaguered banks, after over a year of aggressive rate increases. The labor market has begun to loosen but is still relatively strong with low unemployment and jobless claims, elevated job openings numbers, and a solid track record of jobs added in the last several months. Consumer spending remains healthy, particularly on services such as entertainment, travel, and leisure. Company earnings thus far have been better than feared, with earnings per share (EPS) down less than 1% compared to analyst estimates for a ~6% decline. Volatility has been low, with the VIX “fear index” reaching a three-year low. The equity market appears to buy the argument that the US is headed for a “soft landing” scenario, in which inflation comes down and a recession is avoided.

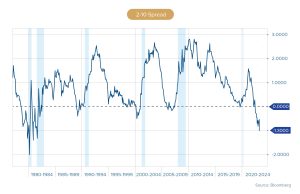

The equity market seems to be brushing off recession concerns, taking a “glass half full” view of the economy….The bond market wholeheartedly disagrees.

The bond market wholeheartedly disagrees. The strongest recession signal offered by the bond market is the deep yield curve inversion. A “normal” yield curve is upward sloping, with shorter dated maturities offering lower yields and longer dated maturities offering higher yields. Today, the bond market is “inverted,” with shorter dated maturities offering higher yields than longer dated maturities. We track the historical spread between the 2-year yield and the 10-year yield, as an inversion between these two points has historically been a reliable leading indicator of an impending recession. The spread tipped into negative/inverted territory on July 6, 2022. It now stands at a full 1.00% inversion, the deepest in about 40 years. The bond market is signaling the belief that the Fed’s rate hike campaign will ultimately lead to an economic recession, which will necessitate aggressive rate cuts on the short end of the curve.

Despite the pause in rate hikes at the June meeting, most Fed officials are forecasting two more 0.25% rate hikes between now and the end of the year. (The bond market is skeptical that the Fed will follow through on these hikes, ostensibly forecasting a recession will hit before year-end.) Fed Chair Jerome Powell continues to reiterate that inflation is a long way from the Fed’s stated target level of 2%. Furthermore, although headline inflation has been cut in half over the last year, core inflation, which strips out the volatile food and energy categories, has barely budged over the last five months, currently sitting at 5.3%. Many attribute this “stickiness” to higher wages due to the tight labor market. It may be difficult to bring core inflation lower without causing further damage to the labor market.

Despite the pause in rate hikes at the June meeting, most Fed officials are forecasting two more 0.25% rate hikes between now and the end of the year. (The bond market is skeptical that the Fed will follow through on these hikes, ostensibly forecasting a recession will hit before year-end.) Fed Chair Jerome Powell continues to reiterate that inflation is a long way from the Fed’s stated target level of 2%. Furthermore, although headline inflation has been cut in half over the last year, core inflation, which strips out the volatile food and energy categories, has barely budged over the last five months, currently sitting at 5.3%. Many attribute this “stickiness” to higher wages due to the tight labor market. It may be difficult to bring core inflation lower without causing further damage to the labor market.

Overall, the forward price-to-earnings ratio of the S&P 500 index stands at 19.4x, compared to a 20-year average of 15.5x. We think equities look a bit expensive at these levels, especially given that higher yields in the bond market offer an attractive alternative. The TINA (“there is no alternative”) mantra of 2021 no longer rings true, given 5%+ yields in the bond market. While we track the two primary recession indicators closely, we remained disciplined on valuation, favoring equity market sectors and companies that are more defensive in nature. We are also beginning to extend duration slightly in bond market allocations, supplementing short-duration Treasury ladders that we have constructed in client portfolios by adding intermediate term investment grade credit to pick up additional yield.

Overall, the forward price-to-earnings ratio of the S&P 500 index stands at 19.4x, compared to a 20-year average of 15.5x. We think equities look a bit expensive at these levels, especially given that higher yields in the bond market offer an attractive alternative. The TINA (“there is no alternative”) mantra of 2021 no longer rings true, given 5%+ yields in the bond market. While we track the two primary recession indicators closely, we remained disciplined on valuation, favoring equity market sectors and companies that are more defensive in nature. We are also beginning to extend duration slightly in bond market allocations, supplementing short-duration Treasury ladders that we have constructed in client portfolios by adding intermediate term investment grade credit to pick up additional yield.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Capital Management, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

Receive our next post in your inbox.