Nelson Capital Management

All Eyes on the Consumer

Asset Management, Quarterly Commentary

October 2, 2023

All Eyes on the Consumer

Is a recession just around the corner, or have we avoided one completely? After one of the most aggressive rate hike cycles in decades, the “hard or soft landing” debate continues. So far, we have not seen obvious signs that the U.S. economy is cracking. Inflation has steadily retreated, moving closer to the Fed’s ultimate 2% target. We see a series of balances. The labor market has cooled, but remained strong enough to keep most people gainfully employed. Company earnings have surprised to the upside, even though profit growth is slowing. Consumer behavior has normalized, but most companies are cautiously optimistic about the resiliency in consumer spending. Delinquencies have ticked higher, but only to the point where they are now in line with pre-pandemic levels.

The belief that the U.S. will avoid a recession (i.e., the “soft landing scenario”) is based on the strong labor market supporting the economy while inflation is continuing to recede. The latest Consumer Price Index data showed headline inflation growing at 3.7% annually, down from a peak of 9% in June of last year. Core inflation, which strips out the volatile food and energy categories, was 4.35%. This measure has been stickier, but it has declined steadily since March. Meanwhile, unemployment remains historically low at 3.8%. Job openings, though down from a peak of 12 million, are still at around 8.8 million, well above the 20-year average level of about 5 million. The soft landing camp also points out that we may be experiencing “rolling recessions.” In this scenario, an overall recession is avoided because various industries and markets take turns experiencing weakness, rather than everything falling apart simultaneously. This hypothesis is supported by the fact that housing and manufacturing are beginning to recover, just as the consumer looks poised to pull back on leisure spending.

The belief that the U.S. will avoid a recession (i.e., the “soft landing scenario”) is based on the strong labor market supporting the economy while inflation is continuing to recede. The latest Consumer Price Index data showed headline inflation growing at 3.7% annually, down from a peak of 9% in June of last year. Core inflation, which strips out the volatile food and energy categories, was 4.35%. This measure has been stickier, but it has declined steadily since March. Meanwhile, unemployment remains historically low at 3.8%. Job openings, though down from a peak of 12 million, are still at around 8.8 million, well above the 20-year average level of about 5 million. The soft landing camp also points out that we may be experiencing “rolling recessions.” In this scenario, an overall recession is avoided because various industries and markets take turns experiencing weakness, rather than everything falling apart simultaneously. This hypothesis is supported by the fact that housing and manufacturing are beginning to recover, just as the consumer looks poised to pull back on leisure spending.

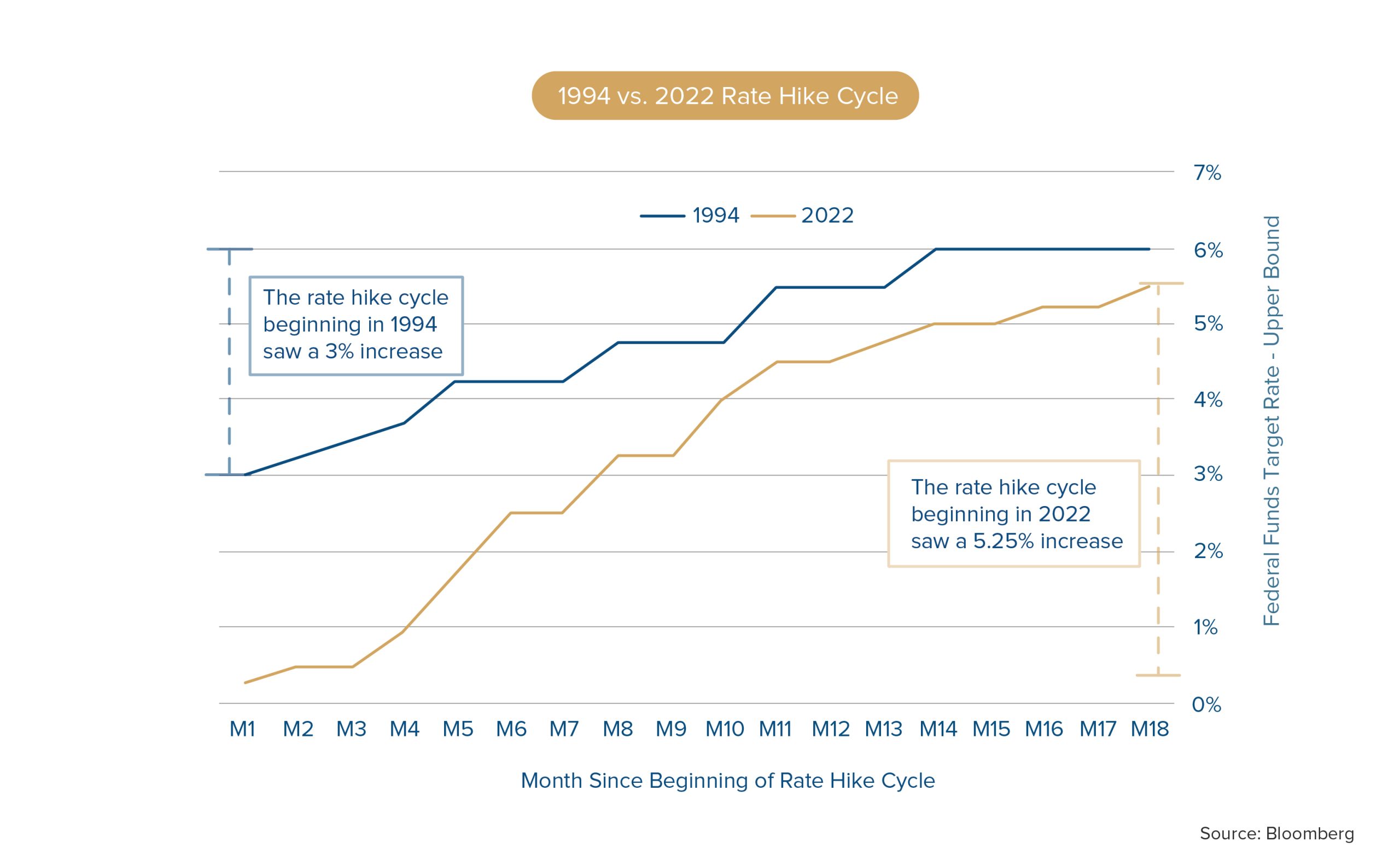

In the last 75 years, we only have one historical example of a soft landing: 1995. The Fed Funds Target rate went from 3% in December 1993 to 6% in March 1995. Today, the Fed is expected to increase rates by 0.25% one more time in November. If they do, it will mean that the Fed Funds Target rate went from 0% in December 2021 to 5.5% at the end of this year. Although rates in 1995 hit a slightly higher peak level, the Fed only hiked rates by 3 percentage points (300 basis points), compared to 5.50 percentage points (550 basis points) in this cycle. A greater surge in rates tends to inflict more pain on consumers—just ask anyone who is currently trying to finance a new home or car. Alan Blinder, an economist who was the Fed vice chair from 1994 to 1996 commented in a recent Wall Street Journal article that the Fed “steered the economy very expertly, but in addition, we were lucky. Nothing bad happened.”

Something “bad” happened earlier this year (remember Silicon Valley Bank?), but the bulk of the bad news has been overshadowed by excitement over new developments in artificial intelligence and a 14% rise in the S&P 500 (NB: This rise has been driven almost entirely by seven companies—Amazon, Apple, Alphabet, Microsoft, Meta, Nvidia and Tesla—and such a narrow market rally can be precarious). At this point, the bank failures from early March seem like ancient history. What else could go wrong this time that might jeopardize the soft-landing scenario? Recent headlines have focused on disruption in the form of the United Auto Workers strike and a potential government shutdown. The Fed also must now grapple with the effects of higher oil prices, with oil creeping closer to $100 per barrel. Most economists have written off higher energy prices as normal fluctuations in a volatile category. However, the longer higher prices stick around, the more likely it is that they seep into the overall inflation data.

For now, the strong labor market means that most Americans are gainfully employed, but we are concerned that things could spiral into recession quickly if consumers begin aggressively tightening their belts.

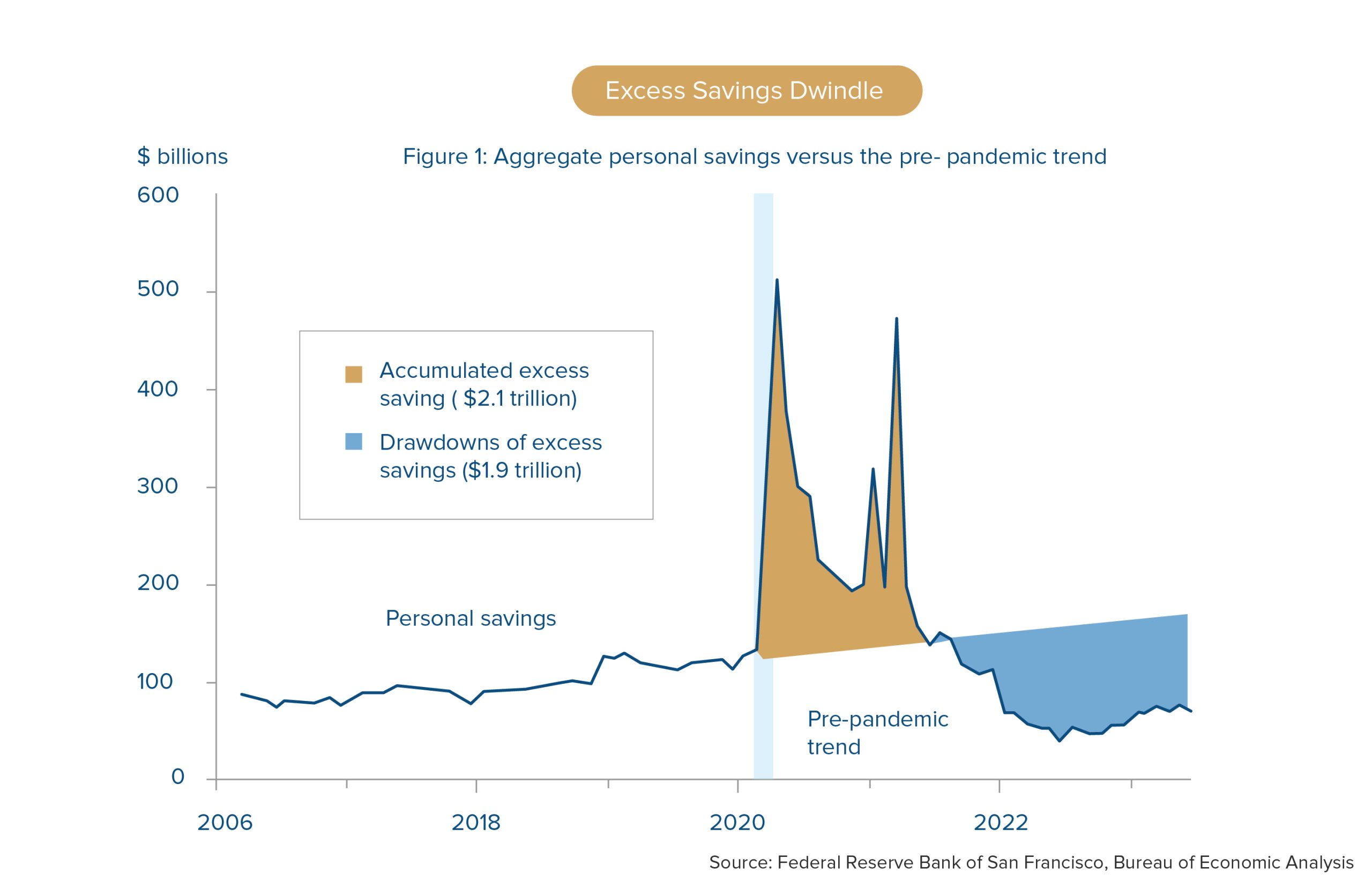

We think the biggest underlying threat to the soft landing scenario would be a sharp pullback in consumer spending, which makes up about two-thirds of GDP. Much of the pandemic-era savings have been spent—first on goods with everyone stuck at home, next on travel when the world finally reopened, and the final iteration of “revenge spending” has gone toward experiences, including high-profile events this summer (e.g., Beyonce’s “Renaissance” tour and Taylor Swift’s “Eras” tour). The SF Fed published a paper in August noting that excess pandemic savings are likely near depletion. Furthermore, this comes at a time when approximately 45 million Americans will need to resume student loan payments, which have been on hold since the depths of the pandemic in 2020. The average monthly payment of such loans is $503, which is about 13% of disposable personal income. For now, the strong labor market means that most Americans are gainfully employed, but we are concerned that things could spiral into recession quickly if consumers begin aggressively tightening their belts.

We are skeptical about the Fed navigating a soft landing. We are looking for signs of weakness in the consumer, which we think may be a harbinger of an impending recession. We are carefully monitoring the data on consumer spending (particularly on interest rate-sensitive, big-ticket items like cars and homes), delinquency rates, and personal savings. We maintain a disciplined approach to equity selection, focusing on companies in defensive sectors that carry a lower valuation. Although we see challenges to the equity market given that inflation-adjusted rates are the highest they have been in over a decade, we continue to find opportunities within the bond market. The fixed income ladders we have built in client portfolios continue to perform well in this rising rate environment, and we believe that it will soon be time to extend durations.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Capital Management, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

Receive our next post in your inbox.