Nelson Capital Management

Grantor Retained Annuity Trusts

Education, Retirement, Taxes, Wealth Management

June 18, 2024

Grantor Retained Annuity Trusts

Grantor Retained Annuity Trusts (GRATs) are used to transfer the future appreciation of an asset out of a Grantor’s estate to his or her heirs while minimizing potential gift taxes. These trusts have been used with rapidly appreciating equities, real estate, and other appreciating assets.

Grantor Retained Annuity Trusts (GRATs) are used to transfer the future appreciation of an asset out of a Grantor’s estate to his or her heirs while minimizing potential gift taxes. These trusts have been used with rapidly appreciating equities, real estate, and other appreciating assets.

Individuals who wish to use a GRAT decide how long the trust will last and how much of the appreciating asset to contribute to the trust. The individual contributing (granting) the assets to the trust is defined as the Grantor.

The Grantor contributes assets that are likely to appreciate substantially while in the trust. Each year, usually on the anniversary of the GRAT’s creation, a portion of the value of the assets contributed, plus a modest minimum annual return stipulated by the IRS, is returned to the Grantor. Estate planning attorneys construct the trust documents and calculate if there is any gift tax liability that might use a part of the Grantor’s lifetime estate exemption using the minimum return required and the term selected by the Grantor. Depending on the interest rate environment and the term of the trust, the portion of the exemption used is usually negligible, if not zero.

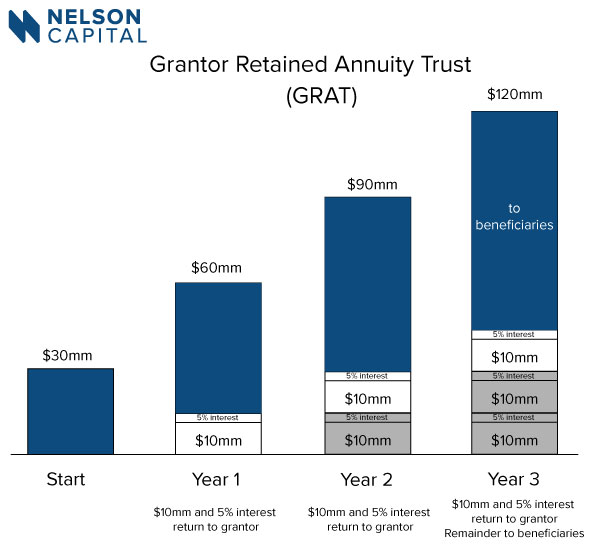

For example, a 3-year GRAT that is funded with 300,000 shares of a stock trading at $100 per share would have a total value upon creation of $30 million worth of stock. The GRAT will return one-third of the contribution value ($10 million) plus interest per year for 3 years. If the stock is trading at $150 per share one year later, then 66,667 shares would return $10 million in value to the Grantor. If the stock is trading at the end of the second year at $200 per share, 50,000 shares would return the next $10 million. If at the end of the third year, the stock is trading at $250, 40,000 shares would return the last $10 million. At the end of the GRAT term, the trust will have returned $30 million of stock for a total of 156,667 shares, leaving 143,333 shares worth $35,833,250 in the GRAT. Those remaining shares are distributed to the beneficiaries. Because the Grantor has received the value of the shares granted, plus interest, the remaining shares are not considered a gift, therefore preserving the Grantor’s lifetime estate tax exemption. The beneficiaries of a GRAT can be either individuals or trust(s) benefiting individuals.

Marketable securities are easily valued, making them ideal for GRATs. Privately-held businesses and real estate require annual appraisals, which adds to the cost of administering a GRAT, but those costs can be very worthwhile with large estates comprised of highly-appreciating assets.

For the GRAT to work, the Grantor must survive the term of the trust. This is often an incentive to keep the term shorter. Sometimes multiple short-term GRATs are established in a series to reduce the risk that GRAT collapses due to the early, untimely passing of the Grantor.

As a Grantor Trust, income generated by the assets while in the trust is taxed to the Grantor. By paying taxes on the income, the Grantor maximizes the wealth transfer.

A benefit of GRATs is that if the contributed asset does not appreciate, at the conclusion of the term, the asset reverts to the Grantor. For example, if a grantor contributes pre-IPO stock to a GRAT but finds that the IPO does not happen, then the Grantor simply retains the shares.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Capital Management, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

Receive our next post in your inbox.