Nelson Capital Management

Disruption and Opportunity

Asset Management, Education, Investment Themes, Quarterly Commentary, The Economy

April 6, 2026

Disruption and Opportunity

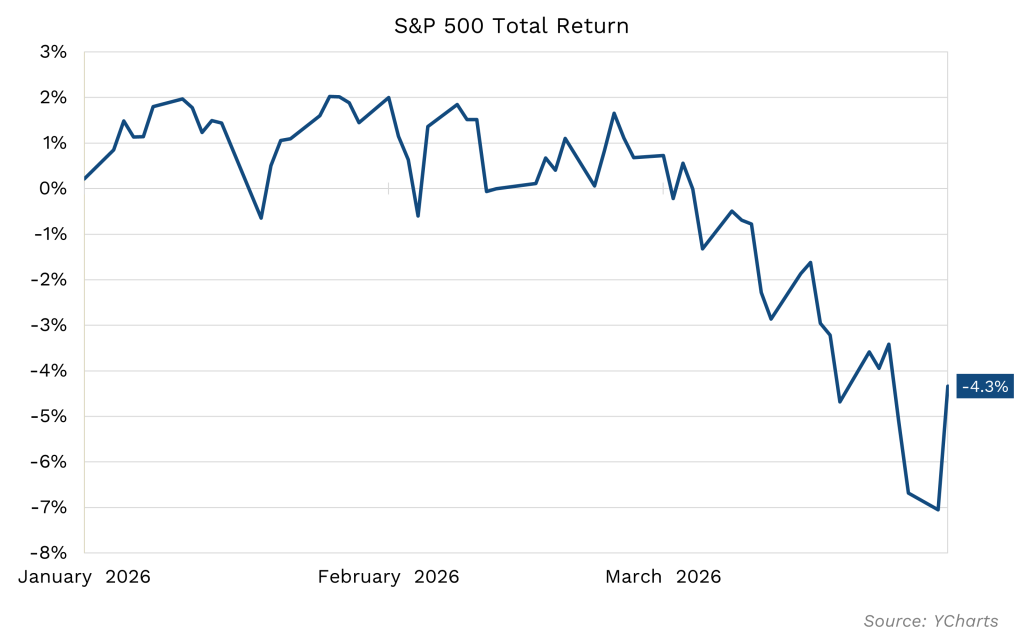

The equity market struggled to find its footing in early 2026, failing to sustain the upward momentum of the previous year. Volatility spiked in January and February as a wave of AI breakthroughs unsettled the software sector, sparking fears that emerging technologies might render established business models obsolete. This anxiety was compounded in late February by the U.S. military action in Iran, which jolted global markets and sent oil prices surging. This double disruption created severe turbulence across global markets.

The equity market struggled to find its footing in early 2026, failing to sustain the upward momentum of the previous year. Volatility spiked in January and February as a wave of AI breakthroughs unsettled the software sector, sparking fears that emerging technologies might render established business models obsolete. This anxiety was compounded in late February by the U.S. military action in Iran, which jolted global markets and sent oil prices surging. This double disruption created severe turbulence across global markets.

By the end of the first quarter, the S&P 500 had retreated 7% from its January 12th peak, while the Nasdaq officially entered correction territory with a decline exceeding 10%. A late March bounce brought the year-to-date decline in the S&P to 3.5%. International equities also softened, though they maintained their relative lead over U.S. markets.

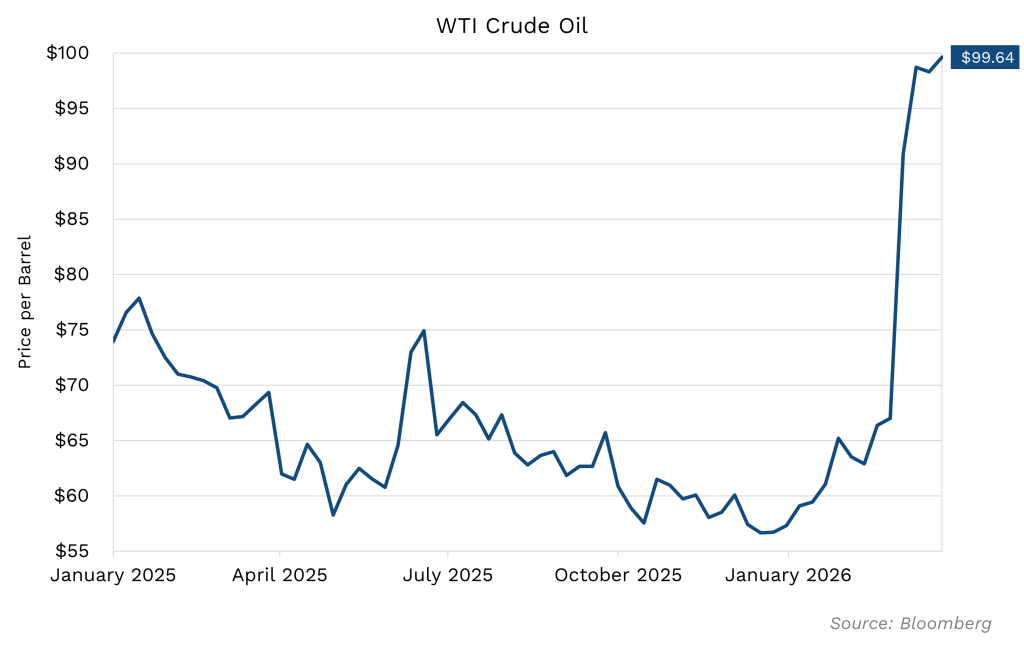

Since the onset of the conflict, the price of Brent Crude oil climbed from approximately $67 to over $110 per barrel. With the Strait of Hormuz effectively closed, roughly one-fifth of the global energy supply remains interrupted. Market prognosticators warn that if the conflict persists and oil prices stay elevated for an extended period, the resulting inflationary pressure could reverse the multi-year downward trend in consumer prices.

Recent jobs reports have underwhelmed in terms of raw headcount creation, but the unemployment rate remains near historic lows. Notably, the Sahm Rule—a key recessionary indicator that triggers when the three-month average unemployment rate rises 0.50% above its 12-month low—has yet to signal an alarm. A sharp decline in immigration has fostered a “no hire, no fire” labor market; firms are reluctant to expand hiring in this uncertain climate, but layoffs have been isolated to a few high-profile instances. Looking ahead, fiscal stimulus from the One Big Beautiful Bill Act (OBBBA) is expected to bolster consumer spending as tax season approaches.

The Federal Reserve remains committed to its dual mandate of price stability and maximum employment. Prior to the geopolitical escalation, the consensus favored a continuation of the rate-cut campaign initiated in 2025. While futures markets originally priced in a 0.50% cut for early 2026, the energy spike has shifted expectations toward a “hold.” Some analysts even suggest the Fed could reverse course and hike rates if higher energy costs begin to flow downstream into broader consumer goods.

Despite the conflict, analysts project S&P 500 earnings growth of approximately 14%, a figure that has actually trended slightly upward since the start of the year. The combination of price declines and rising earnings forecasts has moderated the forward Price-to-Earnings (P/E) ratio to roughly 19.5x, down from a recent high of 23x.

While geopolitical tensions have temporarily sidelined the discourse on AI disruption, these concerns remain a potent latent market force. A paradox has emerged regarding the massive capital expenditures of “hyperscalers”: Amazon, Microsoft, Alphabet, Meta, and Oracle. Investors are currently caught between two contradictory anxieties: the fear that AI is so effective it will displace entire industries, and the suspicion that companies are overspending on technology with unproven long-term value.

Consequently, the market has penalized these hyperscalers, with stock prices retreating 12–28% year-to-date. Some commentators have also predicted a scenario of mass unemployment driven by AI job destruction, although we remain optimistic. This is because historically, technological transformations serve as catalysts for “creative destruction,” displacing certain roles while simultaneously generating new, more productive employment opportunities.

Despite the conflict, analysts project S&P 500 earnings growth of approximately 14%, a figure that has actually trended slightly upward since the start of the year. The combination of price declines and rising earnings forecasts has moderated the forward Price-to-Earnings (P/E) ratio to roughly 19.5x, down from a recent high of 23x.

Traditionally, geopolitical shocks have offered attractive entry points. A Deutsche Bank study of 30 major events since 1939 found an average peak-to-trough decline of just 4.4%, with a typical recovery period of 14 to 18 days. While the scale of the current oil shock is significant, the approaching midterm elections suggest the administration will be highly motivated to find a resolution, whether through diplomatic channels or further action to reopen global trade routes.

We remain committed to the diversification strategies outlined in last quarter’s commentary. Beyond maintaining broad market exposure, we are ensuring clients have the liquidity required for near-term cash needs and are diligently rebalancing portfolios to align with agreed-upon asset allocation targets.

The opinions expressed in this post are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual. It is only intended to provide education about the financial industry. Individual investment positions discussed should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. Please remember that investing involves risk of loss of principal and capital. Nelson Capital Management, LLC is a registered investment adviser with the U.S. Securities and Exchange Commission. No advice may be rendered by Nelson Capital Management, LLC unless a client service agreement is in place. Likes and dislikes are not considered an endorsement for our firm.

Receive our next post in your inbox.