Nelson Capital Management

The purchase of a home is a significant financial event, especially for the first time. In the Bay Area, homes can be prohibitively expensive. Without family help, first time buyers can be priced out of the market. There are several tools that wealthy parents or grandparents can use to assist a younger generation accomplish their goal of owing their own home. Below, we describe one such approach that involves phased gifting, which enables a young buyer to purchase a home at a price point that may otherwise be out of reach.

For this example, we will consider a young buyer looking to purchase a home with a $1,600,000 price point.

Phase One: Annual Gifting

This first phase begins well in advance of the identification of a property. Per the IRS, any person may gift another individual $19,000 per year (calendar year 2026 amount). This amount, called the annual gift exclusion, is an irrevocable gift and does not incur a tax to either the individual making the gift or to the recipient.

By utilizing this annual gift exclusion, each parent, grandparent and others can gift $19,000 to minor children or young adults. If these gifts are ongoing, the funds that accumulate can become substantial. Nelson Capital, in coordination with estate planning counsel, often recommends that parents consider establishing an irrevocable trust, especially for minors, that utilize a “Crummey right” to create a present interest.

Example: Wife and husband establish an irrevocable trust for the benefit of their 16-year-old child. Every year, they gift $19,000 each ($38,000 total) to this trust. When the child turns 25 years old, the parents have accumulated $380,000 in gifted value (10 years x $38,000), plus any portfolio return, to a trust for the benefit of their child. The assets held within the irrevocable trust can be utilized for a wide range of uses. The accumulated funds can be used to help the child for purchase a home, start a business and or pay for higher education. If the funds remain unused, the trust would ultimately dissolve and be distributed to the child for their discretionary use.

Example: Wife and husband establish an irrevocable trust for the benefit of their 16-year-old child. Every year, they gift $19,000 each ($38,000 total) to this trust. When the child turns 25 years old, the parents have accumulated $380,000 in gifted value (10 years x $38,000), plus any portfolio return, to a trust for the benefit of their child. The assets held within the irrevocable trust can be utilized for a wide range of uses. The accumulated funds can be used to help the child for purchase a home, start a business and or pay for higher education. If the funds remain unused, the trust would ultimately dissolve and be distributed to the child for their discretionary use.

Phase Two: Home Purchase

When the buyer is ready to purchase a home, the funds in the irrevocable trust can be used as a down payment. In some cases, the accumulated funds may be enough support to accomplish the home purchase goal. As home prices have increased, even with down payment help, many children will still need parental help to qualify for a loan. They can get this help by asking mom or dad to cosign on a bank loan. This presents an additional gifting opportunity. In our example, the child has identified a home to purchase with their spouse for $1,600,000. The irrevocable trust has accumulated $400,000 (gift value plus appreciation). In agreement with the terms of the irrevocable trust, the funds are released to assist with a home purchase. The parents could offer to match the $400,000 and then co-sign on a loan of $800,000 for example. This allows the joint purchase of the home as “tenants in common”.

Home Purchase Price: $1,600,000

FUND SOURCES:

Child’s contribution from trust distribution: $400,000 (25.0%)

Parents’ contribution from personal assets: $400,000 (25.0%)

Parents’ participation as cosigners of loan: $800,000 (50.0%)

At this point it is recommended that the child and parents draft and enter into a tenants in common agreement (“TIC”). A TIC stipulates the ownership of the property, identifies which party is responsible for making the mortgage payments, taxes and ongoing maintenance. The agreement can stipulate, for example, that the mortgage is carried by the child, increasing the ownership attributable to the child. Parents can still utilize the annual gift exclusion ($19,000 per parent) to help the child with the ongoing mortgage payments, if necessary.

At this point it is recommended that the child and parents draft and enter into a tenants in common agreement (“TIC”). A TIC stipulates the ownership of the property, identifies which party is responsible for making the mortgage payments, taxes and ongoing maintenance. The agreement can stipulate, for example, that the mortgage is carried by the child, increasing the ownership attributable to the child. Parents can still utilize the annual gift exclusion ($19,000 per parent) to help the child with the ongoing mortgage payments, if necessary.

In this example, if the child is identified as the mortgage owner, the ownership of the new home would be split 75% to the child and 25% to the parents.

CHILD‘S OWNERSHIP (75%):

$400,000 (from down payment)

$800,000 (mortgage balance)

PARENT’S OWNERSHIP (25%)

The $400,000 contribution by the parents

The $400,000 contribution by the parents at the time the home is purchased is not a gift to the child and therefore it is not taxable to either party.

Phase Three: Discounted Gifting

The child is now living in and enjoying their new home. The parents own a minority interest (25%) in the home, presenting an additional gifting opportunity. The parents have a minority interest in an illiquid real estate asset. They can have a “discount” appraisal done to determine how much of a discount can be applied to this minority interest, which is both illiquid and significantly below 50%. The discount is substantial, normally ranging from 30% to 45% of pro rata market value. In our example, the $400,000 (25%) in the parents’ market value, could be discounted by 40% to $240,000. The discounted value is important as it enables the parents to pass more actual value to their child with a discounted impact on gifting.

In this example, the parents decide to make a significant one-time gift to their child, utilizing the lifetime exclusion ($15 million in 2026 per person) to gift their minority interest of the home to the child. After receiving the discounted appraisal, the parents file to gift their 25% interest in the home, which represents $400,000 in home market value. In the year of the transfer, the parents file a gift tax return indicating a gift value of $240,000. With the gift tax return, completed by their tax preparer along with their annual tax return, they have utilized part of their lifetime exclusion, avoiding any taxable implications for themselves or their child.

In this example, the parents decide to make a significant one-time gift to their child, utilizing the lifetime exclusion ($15 million in 2026 per person) to gift their minority interest of the home to the child. After receiving the discounted appraisal, the parents file to gift their 25% interest in the home, which represents $400,000 in home market value. In the year of the transfer, the parents file a gift tax return indicating a gift value of $240,000. With the gift tax return, completed by their tax preparer along with their annual tax return, they have utilized part of their lifetime exclusion, avoiding any taxable implications for themselves or their child.

Cost considerations:

This phased approach accomplishes the goal of home ownership for the next generation. The process effectively avoids most estate taxes by functioning within the constraints of annual and lifetime gift exclusions. The process does incur some costs, in addition to the normal costs associated with the purchase of a home. These include, but are not limited to:

PHASE ONE:

• Legal fees to establish an irrevocable trust

• Annual tax preparation fees for the irrevocable trust

• Annual trustee tees (a family member is often used, reducing this cost)

PHASE TWO:

• Legal fees to establish tenant in common (“TIC”) agreement

PHASE THREE:

• Cost of discounted appraisal

• Tax services associated with filing of gift tax return

The purchase of a home is a costly endeavor. Commissions paid to real estate professionals, along with title insurance and fees, are significant. Maintenance costs and property taxes should also be considered in determining affordability for a buyer. For buyers who have achieved some stability in their lives, the opportunity to purchase a home can be both emotionally and financially rewarding. Affluent parents can help enable their children realize the goal of home ownership with minimal tax impact.

The opinions expressed in this post are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual. It is only intended to provide education about the financial industry. Individual investment positions discussed should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. Please remember that investing involves risk of loss of principal and capital. Nelson Capital Management, LLC is a registered investment adviser with the U.S. Securities and Exchange Commission. No advice may be rendered by Nelson Capital Management, LLC unless a client service agreement is in place. Likes and dislikes are not considered an endorsement for our firm.

The One Big Beautiful Bill (OBBB), signed into law on July 4, 2025, is one of the most sweeping tax reforms in years. While it touches households across the income spectrum, its most meaningful changes impact high-net-worth individuals and families. From income tax stability to estate planning opportunities, the bill creates both advantages and planning opportunities.

Tax Rates Locked In

The OBBB locks in the current seven-bracket system: 10%, 12%, 22%, 24%, 32%, 35% and 37%. Prior to this law, those brackets were set to sunset in 2025, which would have meant higher rates across the board.

For high earners, the permanence of today’s rates removes a layer of uncertainty. That makes it easier to time things like Roth conversions, trust distributions, and large income events.

Bigger Standard Deduction

The bill makes permanent the larger standard deduction established under the Tax Cuts and Jobs Act (TCJA): $31,500 for married couples and $15,750 for single filers in 2025.

In addition, individuals who are age 65 or older can claim an additional deduction of $6,000 on top of the standard deduction.

For high-net-worth taxpayers, this raises the bar for when deductions like mortgage interest, state taxes, and charitable gifts provide an incremental benefit — making bunching strategies more relevant.

Estate & Gift Breaks

Estate & Gift Breaks

The exemption for estate and gift tax climbs to $15 million per person and $30 million per couple in 2026, indexed for inflation.

This permanently changes the estate planning conversation, giving families more room to transfer wealth without being forced into rushed strategies.

SALT Relief — With Limits

The state and local tax (SALT) deduction cap rises from $10,000 to $40,000 through 2029.

But once income exceeds $500,000, the deduction begins phasing down, never falling below $10,000. Managing income levels will matter for those hoping to maximize the benefit.

AMT Exemption Permanent

The Alternative Minimum Tax (AMT) exemption from the TCJA has been permanently extended up to $88,100 for single filers and $137,00 for joint filers in 2025. However, the exemption phaseout threshold will be reduced to $500,000 for individuals and $1,000,000 for couples and phase-out rate increases from 25% to 50%.

Giving Gets Trickier

Charitable contributions remain deductible, but starting in 2026, itemizers face a 0.5% AGI floor and the top tax benefit for deductions drops from 37% to 35%.

This will push many donors to rethink timing and structure, with donor-advised funds and qualified charitable distributions becoming more valuable.

529s Open Up

Families can now use up to $20,000 per year from 529 plans for K–12 tuition. The list of qualified expenses also expands to cover tutoring, test prep, dual-enrollment, licensing exams, and credentialing programs.

Business Wins

- QBI Deduction: The 20% pass-through deduction is permanent.

- QSBS: Exclusion rises to $15 million, with bigger breaks for longer holding periods.

- Expensing: 100% bonus depreciation returns; Section 179 cap set at $2.5 million.

These provisions tilt heavily toward business owners and investors looking to reinvest or transition efficiently.

Takeaways

The Big Beautiful Bill locks in rates, boosts estate exemptions, and expands business incentives. At the same time, the larger standard deduction, SALT, AMT, charitable giving rules, and 529 changes require fresh planning. While many provisions are labeled “permanent,” tax laws rarely are.

The opinions expressed in this post are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual. It is only intended to provide education about the financial industry. Individual investment positions discussed should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. Please remember that investing involves risk of loss of principal and capital. Nelson Capital Management, LLC is a registered investment adviser with the U.S. Securities and Exchange Commission. No advice may be rendered by Nelson Capital Management, LLC unless a client service agreement is in place. Likes and dislikes are not considered an endorsement for our firm.

No one wants to talk about death or the fact that it can happen to anyone at any time. It is a morbid subject to discuss, but it is also a vital conversation to have with our loved ones. If we do not take steps to prepare for our departure, we risk leaving our executor and beneficiaries in a difficult position where they must piece together information while grieving. Here are some reminders to help ease the burden of estate settlement:

Create a Will/Trust

A will is a legal document that lets you decide what happens to your estate after you die. If an individual dies without a will, a local probate court will choose who receives their property and other assets.

Is Probate Required?

The probate process is the legal method for administering and distributing a deceased person’s estate. Probate can be avoided if the decedent’s assets are held in a trust or their accounts are titled properly. Depending on the state you live in, most estate attorneys recommend avoiding probate as the process can be expensive and lengthy (for example, in California it can take a year or more to clear probate).

The probate process is the legal method for administering and distributing a deceased person’s estate. Probate can be avoided if the decedent’s assets are held in a trust or their accounts are titled properly. Depending on the state you live in, most estate attorneys recommend avoiding probate as the process can be expensive and lengthy (for example, in California it can take a year or more to clear probate).

Assets titled in the following will avoid probate:

- Trusts

- Payable on death (POD)

- Transfer on death (TOD)

- Joint tenancy with right of survivorship

- Retirement plans (IRA, Roth, 401k, pensions, etc. with designated beneficiaries)

- Life insurance

Prepare an Advance Health Care Directive

An advance health care directive is a legal document that outlines how decisions should be made about your medical care if you are ever unable to make those decisions yourself. Part of the directive is nominating someone to have medical power of attorney to make decisions on your behalf. The power of attorney will go into effect only after your doctor deems you incapacitated.

Nominate a Guardian for Minor Children

If you are a parent, you can use your will/trust to nominate a guardian for your minor children. The surviving parent will usually get sole legal custody if one parent dies. However, in the tragic scenario that both parents pass, having a guardian nominated in your will/trust is crucial. A guardian will be responsible for all your children’s daily needs, including food, housing, health care, education, and clothing. If you do not nominate a guardian in your will/trust, a court will have to choose one for you.

Name an Executor

An executor is the person or entity named by the deceased person in a will to administer their estate. If a person has a trust, the executor is referred to as the successor trustee. Being nominated as an executor/trustee can be an honor, but the responsibilities can be substantial. The executor assumes the powers and fiduciary duties necessary to comply with both the terms of the will or trust and the legal requirements imposed by the state.

The time immediately after the death of a loved one can involve a lot of expenses. There may be hospital bills and burial costs, in addition to regular bills like housing expenses and utility bills. If financial assets like bank accounts are held in an individual’s name without any instructions at death, that money may be untouchable for an extended period and until the bank receives legal documents and a death certificate. Opening a joint account or adding a payable at death (POD) feature can give the executor quick access to funds.

Your executor should be able to access the following documents:

Financial Documents

- Tax returns (both federal and state)

- Wills and trust documents

- Beneficiary designations (for IRAs, 401k and qualified retirement plans)

- Bank account statements

- Brokerage account statements

- Credit card statements

- Life insurance policies

- Social security documents

- Passwords (for phones, computers, and online accounts)

Real Estate Documents

- Title papers

- Purchase and renovation documents

- Mortgage agreements

- Home equity loan documents

Other Documents (if applicable)

- Business financial statements

- Promissory notes owed by family or third parties

- Auto registrations

- List of valuables (antiques, artwork, collectible, jewelry)

- Safety deposit box key

Other Important To-Dos for an Executor

- Arrange the funeral or celebration of life

- Publish obituary and notify friends

- Stop all unnecessary expenses such as subscriptions, medical insurance and credit cards

- Obtain death certificates (typically supplied by the funeral home)

- Complete charitable donations

Obtain an Estate Tax ID (EIN) Number After Death

Your executor will be required to obtain a Tax ID number known as an “employer ID number” or EIN. When someone dies, their assets become the property of their estate. Any income those assets generate is also part of the estate and may trigger the requirements to file an estate income tax return. Form 1041 is required if the estate generates more than $600 in annual gross income. The estate federal tax return is due nine months after death, unless an extension is filed.

Conclusion

Navigating the complexities of estate settlement can be challenging and is a significant time commitment. While an executor or trustee doesn’t need to be a tax or legal expert, seeking professional guidance is highly recommended to ensure the estate is managed effectively and in compliance with estate laws. If you need recommendations, we are familiar with a number of highly regarded estate planning experts.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Capital Management, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

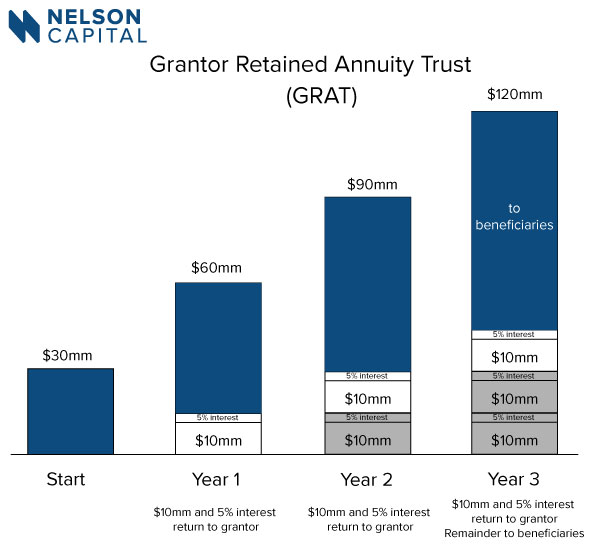

Grantor Retained Annuity Trusts (GRATs) are used to transfer the future appreciation of an asset out of a Grantor’s estate to his or her heirs while minimizing potential gift taxes. These trusts have been used with rapidly appreciating equities, real estate, and other appreciating assets.

Grantor Retained Annuity Trusts (GRATs) are used to transfer the future appreciation of an asset out of a Grantor’s estate to his or her heirs while minimizing potential gift taxes. These trusts have been used with rapidly appreciating equities, real estate, and other appreciating assets.

Individuals who wish to use a GRAT decide how long the trust will last and how much of the appreciating asset to contribute to the trust. The individual contributing (granting) the assets to the trust is defined as the Grantor.

The Grantor contributes assets that are likely to appreciate substantially while in the trust. Each year, usually on the anniversary of the GRAT’s creation, a portion of the value of the assets contributed, plus a modest minimum annual return stipulated by the IRS, is returned to the Grantor. Estate planning attorneys construct the trust documents and calculate if there is any gift tax liability that might use a part of the Grantor’s lifetime estate exemption using the minimum return required and the term selected by the Grantor. Depending on the interest rate environment and the term of the trust, the portion of the exemption used is usually negligible, if not zero.

For example, a 3-year GRAT that is funded with 300,000 shares of a stock trading at $100 per share would have a total value upon creation of $30 million worth of stock. The GRAT will return one-third of the contribution value ($10 million) plus interest per year for 3 years. If the stock is trading at $150 per share one year later, then 66,667 shares would return $10 million in value to the Grantor. If the stock is trading at the end of the second year at $200 per share, 50,000 shares would return the next $10 million. If at the end of the third year, the stock is trading at $250, 40,000 shares would return the last $10 million. At the end of the GRAT term, the trust will have returned $30 million of stock for a total of 156,667 shares, leaving 143,333 shares worth $35,833,250 in the GRAT. Those remaining shares are distributed to the beneficiaries. Because the Grantor has received the value of the shares granted, plus interest, the remaining shares are not considered a gift, therefore preserving the Grantor’s lifetime estate tax exemption. The beneficiaries of a GRAT can be either individuals or trust(s) benefiting individuals.

Marketable securities are easily valued, making them ideal for GRATs. Privately-held businesses and real estate require annual appraisals, which adds to the cost of administering a GRAT, but those costs can be very worthwhile with large estates comprised of highly-appreciating assets.

For the GRAT to work, the Grantor must survive the term of the trust. This is often an incentive to keep the term shorter. Sometimes multiple short-term GRATs are established in a series to reduce the risk that GRAT collapses due to the early, untimely passing of the Grantor.

As a Grantor Trust, income generated by the assets while in the trust is taxed to the Grantor. By paying taxes on the income, the Grantor maximizes the wealth transfer.

A benefit of GRATs is that if the contributed asset does not appreciate, at the conclusion of the term, the asset reverts to the Grantor. For example, if a grantor contributes pre-IPO stock to a GRAT but finds that the IPO does not happen, then the Grantor simply retains the shares.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Capital Management, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

In response to the increasing number of financial fraud cases against seniors, regulators have implemented new rules to protect older clients. SEC and FINRA rules require financial advisors to ask their clients if they would like to designate a person to be contacted in the event that the advisor suspects fraud or mental decline.

What is a “trusted contact person?”

A trusted contact is someone who Nelson Roberts Investment Advisors can get in touch with to:

A trusted contact is someone who Nelson Roberts Investment Advisors can get in touch with to:

• Address possible or suspected financial exploitation involving your account;

• Confirm your contact information in case we have trouble reaching you;

• Confirm if there is someone acting as a legal guardian, an executor, a trustee, or holder of a power of attorney; or

• Determine your mental or physical health status.

It is important to note that your trusted contact does not have authority to access your account or make transactions on your behalf. Instead, the trusted contact’s role is to help us contact you; to provide the identity of any legal guardian, executor, trustee, or holder of a power of attorney; or to help us guard against financial exploitation.

Why should I add a trusted contact person to my account? Investment advisors often serve as the first line of defense when it comes to cases of possible financial exploitation. A trusted contact person is another resource to help protect you and your loved ones against financial abuse. A trusted contact person is another way of protecting your personal assets when something unexpected happens in your life. It adds an additional level of security to your account.

Who can be a trusted contact?

Trusted contacts are usually family members or close friends— people you trust and who are likely to be in the best position to know your current situation. A trusted contact must be at least eighteen years old. Please note, a trusted contact person need not be the same as someone who acts as a representative under a power of attorney.

Part of your financial planning should include identifying people who Nelson Roberts Investment Advisors can contact if we suspect you are a target of financial exploitation or if we see signs suggesting that you are becoming unable to manage your finances alone. Please contact us if you wish to add a trusted contact person to your account.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Roberts Investment Advisors, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Roberts Investment Advisors, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

In the early part of this century, lax lending standards contributed to a housing bubble that ultimately led to the credit default swap market collapse, nearly bankrupting the U.S. banking system. In response to the crisis, the government enacted substantial banking regulations in order to prevent the recurrence of such dramatic market events. As a result, the banking industry is now mired in with process and red tape that makes obtaining a loan a time-intensive ordeal. For a borrower that lacks income, even temporarily, or for a borrower in the midst of a life transition, obtaining loans from traditional sources can be daunting.

In the early part of this century, lax lending standards contributed to a housing bubble that ultimately led to the credit default swap market collapse, nearly bankrupting the U.S. banking system. In response to the crisis, the government enacted substantial banking regulations in order to prevent the recurrence of such dramatic market events. As a result, the banking industry is now mired in with process and red tape that makes obtaining a loan a time-intensive ordeal. For a borrower that lacks income, even temporarily, or for a borrower in the midst of a life transition, obtaining loans from traditional sources can be daunting.

There are options in the marketplace, such as margin loans or home equity lines, but these solutions carry the burden of bank underwriting or high interest rates.

Many of our clients have benefited from the ability to collateralize securities in their investment portfolios and access lines of credit that can provide timely, inexpensive access to liquidity.

For example, consider a couple getting a divorce, where one of the parties has been awarded the residence and the other has been awarded the $3.0 million portfolio. The individual with the portfolio assets would like to buy a residence of his own, but does not have a recent history of wage income as an individual, making a traditional loan difficult to obtain. The $3.0 million portfolio may also have embedded gains that carry a tax liability.

The individual can obtain a line of credit based on the value of his $3.0 million portfolio. He can:

- Borrow up to 70% of the value of the investment account, up to $2.1 million in this example.

- Pay interest at a competitive variable rate for a five-year term

- Pay interest only on the portion of the line that is used

- Pay back any or all of the line at any time with no prepayment penalty

This line of credit would enable the individual to both purchase a home and keep his portfolio intact until he is able to transition to a traditional banking product. We have helped clients utilize a securities-based line of credit for purposes such as:

- Bridging a loan for the time period between purchasing and selling a home

- Near-term liquidity for estate gifting

- Near-term liquidity for tax planning

A securities-based line of credit can be established in less than three weeks. We welcome the opportunity to discuss this strategy further with you.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Roberts Investment Advisors, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.