Nelson Capital Management

Retirement is one of the most significant transitions in life. It marks the shift from structured days and steady paychecks to a new rhythm centered on personal choice, freedom, and the opportunity to redefine how you want to live. But the very things that make retirement exciting also make it complex. It requires stepping away from predictability and stepping into a chapter where your financial security depends more on past preparation than on future earnings. This mix of freedom and responsibility creates a natural tension between the desire to enjoy your time while ensuring your resources last. That tension becomes even more pronounced when retirement coincides with a market high.

Retiring at a market top can feel like perfect timing. After years of contributions and compounding, your portfolio may be larger than it has ever been. Seeing a high balance can create a powerful sense of readiness. Yet the same market strength that boosts your confidence also introduces meaningful risks. Market peaks are recognizable only in hindsight, and what feels like strong market today could be the start of weaker or volatile returns ahead.

The real challenge begins once you shift from saving to spending. When you retire, you become immediately exposed to sequence-of-returns risk, which is the danger that poor market performance early in retirement can cause long-lasting damage to your portfolio. If withdrawals occur while markets are declining, those losses become permanent, reducing the base from which future returns can compound. Even a portfolio that looks ample at the start of retirement can become strained if the first few years align with a downturn.

This risk is particularly relevant today, because long periods of strong returns often foster complacency. Over the past decade, U.S. equities have delivered performance far above historical averages. But broad market data across more than two centuries shows that extended periods of lower real returns are not unusual. There have been many 30-year spans in which inflation-adjusted stock returns were in the 3-4% range or lower. If the decades ahead resemble any of those periods rather than the recent boom, retirees who based their plans on optimistic assumptions may face shortfalls. Sustaining a consistent level of spending for a 30-year retirement often requires saving 12 to 20 percent of income during working years, depending on eventual real returns.

This risk is particularly relevant today, because long periods of strong returns often foster complacency. Over the past decade, U.S. equities have delivered performance far above historical averages. But broad market data across more than two centuries shows that extended periods of lower real returns are not unusual. There have been many 30-year spans in which inflation-adjusted stock returns were in the 3-4% range or lower. If the decades ahead resemble any of those periods rather than the recent boom, retirees who based their plans on optimistic assumptions may face shortfalls. Sustaining a consistent level of spending for a 30-year retirement often requires saving 12 to 20 percent of income during working years, depending on eventual real returns.

Spending patterns also play a more important role than many realize. Although people often assume retirement will cost less, research shows most retirees spend nearly as much as they did while working, and many spend more in their early, active years. Those who spend significantly less usually do so out of necessity, not preference. Beginning retirement at a market high does not change the need for disciplined spending.

Given these risks, the way you structure your withdrawal plan becomes essential. Two tools can help reduce vulnerability to market timing and early downturns: the bucket strategy and dynamic withdrawal rules.

The bucket strategy separates your portfolio into segments according to time horizon. One bucket holds three to five years of essential spending in cash or short-term bonds shielding your lifestyle from equity market volatility. A second bucket focuses on intermediate-term stability, and a third holds longer-term growth assets, such as equities. This framework helps you avoid selling stocks at unfavorable times by giving you dedicated reserves to draw from during market declines. It also creates a more predictable system for replenishing each bucket over time.

Dynamic withdrawal rules add another layer of resilience. Unlike fixed withdrawal systems, dynamic approaches adjust spending based on market conditions. Guardrail methods allow higher spending when markets perform well and reduce withdrawals slightly when portfolio balances fall below predetermined thresholds. Percentage-based withdrawal methods tie annual spending to a set percentage of the portfolio, ensuring sustainability even during extended downturns. Even simple strategies, such as pausing inflation adjustments or trimming discretionary spending during weak markets, can meaningfully extend portfolio longevity.

Retiring at a market top is neither inherently good nor inherently risky. It offers genuine advantages, but it also requires planning and realistic expectations. The success of retirement depends less on guessing the perfect moment to leave the workforce and more on building a plan capable of navigating whatever markets deliver next. Confidence at the peak is valuable, but resilience afterward matters far more.

The opinions expressed in this post are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual. It is only intended to provide education about the financial industry. Individual investment positions discussed should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. Please remember that investing involves risk of loss of principal and capital. Nelson Capital Management, LLC is a registered investment adviser with the U.S. Securities and Exchange Commission. No advice may be rendered by Nelson Capital Management, LLC unless a client service agreement is in place. Likes and dislikes are not considered an endorsement for our firm.

Required Minimum Distributions (RMDs) are the minimum amount that a retiree must withdraw from retirement accounts each year. They apply to traditional IRAs, SEP IRAs, SIMPLE IRAS, 401(k)s and 403(b)s. They do not apply to Roth IRAs or Designated Roth accounts in a 401(k) or 403(b). The distribution is taxed as ordinary income in the year it is withdrawn.

The SECURE Act of 2020 pushed the age at which you are required to start taking RMDs from 70½ to 72. SECURE 2.0 pushed it further to ages 73-75 depending on the year in which you are born. The calculation for the amount of an RMD is based on the account balance at the end of the previous year and a life expectancy factor determined by IRS tables. It starts around 4% of the account balance and increases as life expectancy decreases. The first RMD must be taken by April 1st of the year after the account owner turns the applicable RMD age and future RMDs must be taken by December 31st of each year. The penalty for failing to take an RMD is 25% but can be reduced to 10% if corrected within two years.

The SECURE Act of 2020 pushed the age at which you are required to start taking RMDs from 70½ to 72. SECURE 2.0 pushed it further to ages 73-75 depending on the year in which you are born. The calculation for the amount of an RMD is based on the account balance at the end of the previous year and a life expectancy factor determined by IRS tables. It starts around 4% of the account balance and increases as life expectancy decreases. The first RMD must be taken by April 1st of the year after the account owner turns the applicable RMD age and future RMDs must be taken by December 31st of each year. The penalty for failing to take an RMD is 25% but can be reduced to 10% if corrected within two years.

The rules around RMDs for Inherited IRAs were changed significantly by the SECURE Act. Prior to 2020, non-spouse beneficiaries were able to stretch distributions from an Inherited IRA over their lifetime with RMDs based on their life expectancy. The SECURE Act instituted the 10-Year Rule where non-spouse beneficiaries must withdraw the full balance of the Inherited IRA within 10 years. IRAs inherited prior to 2020 are grandfathered into the old rules and not subject to the 10-Year Rule. Certain types of beneficiaries, known as Eligible Designed Beneficiaries (EDBs), are also not subject to the 10-Year Rule and may take RMDs based on their life expectancy. These beneficiaries include the spouse or minor children of the deceased IRA owner, disabled or chronically ill individuals, and individuals not more than 10 years younger than the IRA owner. Minor children are subject to the 10-Year Rule once they reach the age of majority.

The original law did not offer guidance on RMDs for Inherited IRAs but the IRS recently issued final rules stating RMDs must be taken from Inherited IRAs each year throughout the 10-year period. However, this does not go into effect until 2025. This applies to both Inherited IRAs and Inherited Roth IRA. Withdrawals of contributions from Inherited Roth IRAs are tax free. Withdrawals of earnings from an Inherited Roth IRA are also tax free unless the account is less than 5-years old at the time of the withdrawal.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Capital Management, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

No one wants to talk about death or the fact that it can happen to anyone at any time. It is a morbid subject to discuss, but it is also a vital conversation to have with our loved ones. If we do not take steps to prepare for our departure, we risk leaving our executor and beneficiaries in a difficult position where they must piece together information while grieving. Here are some reminders to help ease the burden of estate settlement:

Create a Will/Trust

A will is a legal document that lets you decide what happens to your estate after you die. If an individual dies without a will, a local probate court will choose who receives their property and other assets.

Is Probate Required?

The probate process is the legal method for administering and distributing a deceased person’s estate. Probate can be avoided if the decedent’s assets are held in a trust or their accounts are titled properly. Depending on the state you live in, most estate attorneys recommend avoiding probate as the process can be expensive and lengthy (for example, in California it can take a year or more to clear probate).

The probate process is the legal method for administering and distributing a deceased person’s estate. Probate can be avoided if the decedent’s assets are held in a trust or their accounts are titled properly. Depending on the state you live in, most estate attorneys recommend avoiding probate as the process can be expensive and lengthy (for example, in California it can take a year or more to clear probate).

Assets titled in the following will avoid probate:

- Trusts

- Payable on death (POD)

- Transfer on death (TOD)

- Joint tenancy with right of survivorship

- Retirement plans (IRA, Roth, 401k, pensions, etc. with designated beneficiaries)

- Life insurance

Prepare an Advance Health Care Directive

An advance health care directive is a legal document that outlines how decisions should be made about your medical care if you are ever unable to make those decisions yourself. Part of the directive is nominating someone to have medical power of attorney to make decisions on your behalf. The power of attorney will go into effect only after your doctor deems you incapacitated.

Nominate a Guardian for Minor Children

If you are a parent, you can use your will/trust to nominate a guardian for your minor children. The surviving parent will usually get sole legal custody if one parent dies. However, in the tragic scenario that both parents pass, having a guardian nominated in your will/trust is crucial. A guardian will be responsible for all your children’s daily needs, including food, housing, health care, education, and clothing. If you do not nominate a guardian in your will/trust, a court will have to choose one for you.

Name an Executor

An executor is the person or entity named by the deceased person in a will to administer their estate. If a person has a trust, the executor is referred to as the successor trustee. Being nominated as an executor/trustee can be an honor, but the responsibilities can be substantial. The executor assumes the powers and fiduciary duties necessary to comply with both the terms of the will or trust and the legal requirements imposed by the state.

The time immediately after the death of a loved one can involve a lot of expenses. There may be hospital bills and burial costs, in addition to regular bills like housing expenses and utility bills. If financial assets like bank accounts are held in an individual’s name without any instructions at death, that money may be untouchable for an extended period and until the bank receives legal documents and a death certificate. Opening a joint account or adding a payable at death (POD) feature can give the executor quick access to funds.

Your executor should be able to access the following documents:

Financial Documents

- Tax returns (both federal and state)

- Wills and trust documents

- Beneficiary designations (for IRAs, 401k and qualified retirement plans)

- Bank account statements

- Brokerage account statements

- Credit card statements

- Life insurance policies

- Social security documents

- Passwords (for phones, computers, and online accounts)

Real Estate Documents

- Title papers

- Purchase and renovation documents

- Mortgage agreements

- Home equity loan documents

Other Documents (if applicable)

- Business financial statements

- Promissory notes owed by family or third parties

- Auto registrations

- List of valuables (antiques, artwork, collectible, jewelry)

- Safety deposit box key

Other Important To-Dos for an Executor

- Arrange the funeral or celebration of life

- Publish obituary and notify friends

- Stop all unnecessary expenses such as subscriptions, medical insurance and credit cards

- Obtain death certificates (typically supplied by the funeral home)

- Complete charitable donations

Obtain an Estate Tax ID (EIN) Number After Death

Your executor will be required to obtain a Tax ID number known as an “employer ID number” or EIN. When someone dies, their assets become the property of their estate. Any income those assets generate is also part of the estate and may trigger the requirements to file an estate income tax return. Form 1041 is required if the estate generates more than $600 in annual gross income. The estate federal tax return is due nine months after death, unless an extension is filed.

Conclusion

Navigating the complexities of estate settlement can be challenging and is a significant time commitment. While an executor or trustee doesn’t need to be a tax or legal expert, seeking professional guidance is highly recommended to ensure the estate is managed effectively and in compliance with estate laws. If you need recommendations, we are familiar with a number of highly regarded estate planning experts.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Capital Management, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

Grantor Retained Annuity Trusts (GRATs) are used to transfer the future appreciation of an asset out of a Grantor’s estate to his or her heirs while minimizing potential gift taxes. These trusts have been used with rapidly appreciating equities, real estate, and other appreciating assets.

Grantor Retained Annuity Trusts (GRATs) are used to transfer the future appreciation of an asset out of a Grantor’s estate to his or her heirs while minimizing potential gift taxes. These trusts have been used with rapidly appreciating equities, real estate, and other appreciating assets.

Individuals who wish to use a GRAT decide how long the trust will last and how much of the appreciating asset to contribute to the trust. The individual contributing (granting) the assets to the trust is defined as the Grantor.

The Grantor contributes assets that are likely to appreciate substantially while in the trust. Each year, usually on the anniversary of the GRAT’s creation, a portion of the value of the assets contributed, plus a modest minimum annual return stipulated by the IRS, is returned to the Grantor. Estate planning attorneys construct the trust documents and calculate if there is any gift tax liability that might use a part of the Grantor’s lifetime estate exemption using the minimum return required and the term selected by the Grantor. Depending on the interest rate environment and the term of the trust, the portion of the exemption used is usually negligible, if not zero.

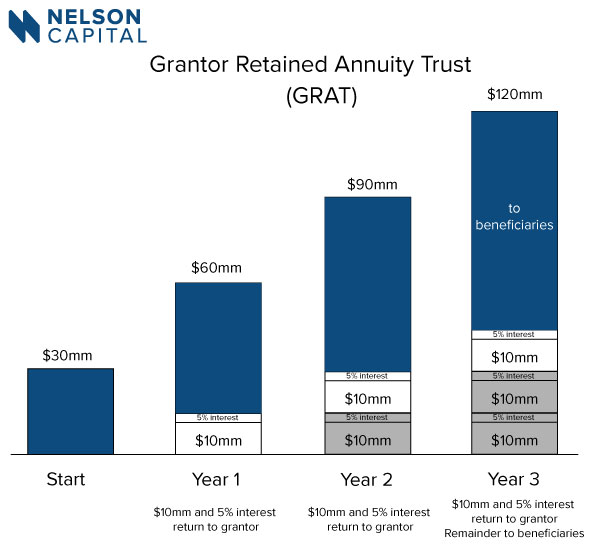

For example, a 3-year GRAT that is funded with 300,000 shares of a stock trading at $100 per share would have a total value upon creation of $30 million worth of stock. The GRAT will return one-third of the contribution value ($10 million) plus interest per year for 3 years. If the stock is trading at $150 per share one year later, then 66,667 shares would return $10 million in value to the Grantor. If the stock is trading at the end of the second year at $200 per share, 50,000 shares would return the next $10 million. If at the end of the third year, the stock is trading at $250, 40,000 shares would return the last $10 million. At the end of the GRAT term, the trust will have returned $30 million of stock for a total of 156,667 shares, leaving 143,333 shares worth $35,833,250 in the GRAT. Those remaining shares are distributed to the beneficiaries. Because the Grantor has received the value of the shares granted, plus interest, the remaining shares are not considered a gift, therefore preserving the Grantor’s lifetime estate tax exemption. The beneficiaries of a GRAT can be either individuals or trust(s) benefiting individuals.

Marketable securities are easily valued, making them ideal for GRATs. Privately-held businesses and real estate require annual appraisals, which adds to the cost of administering a GRAT, but those costs can be very worthwhile with large estates comprised of highly-appreciating assets.

For the GRAT to work, the Grantor must survive the term of the trust. This is often an incentive to keep the term shorter. Sometimes multiple short-term GRATs are established in a series to reduce the risk that GRAT collapses due to the early, untimely passing of the Grantor.

As a Grantor Trust, income generated by the assets while in the trust is taxed to the Grantor. By paying taxes on the income, the Grantor maximizes the wealth transfer.

A benefit of GRATs is that if the contributed asset does not appreciate, at the conclusion of the term, the asset reverts to the Grantor. For example, if a grantor contributes pre-IPO stock to a GRAT but finds that the IPO does not happen, then the Grantor simply retains the shares.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Capital Management, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

The SECURE ACT 2.0, signed into law December 29, 2022, made several rule changes that impact retirees and those saving for retirement. The provisions of the retirement package were included in a spending bill that contains 4,155 pages and it builds on the first SECURE ACT which was approved by Congress in 2019.

The SECURE ACT 2.0, signed into law December 29, 2022, made several rule changes that impact retirees and those saving for retirement. The provisions of the retirement package were included in a spending bill that contains 4,155 pages and it builds on the first SECURE ACT which was approved by Congress in 2019.

Here are the key takeaways:

- The age to start taking RMDs increases to age 73 in 2023 and to 75 in 2033.

The most notable provision of this bill from a financial planning perspective is the increase in the age at which individuals must begin taking required minimum distributions (RMDs) from their retirement account from age 72 to 73. The new RMD age applies to anyone who turns 72 on or after January 1, 2023. In 2033, the RMD age will increase again to 75.

- The penalty for failing to take an RMD will decrease to 25% of the RMD amount, from 50% currently, and 10% if corrected in a timely manner for IRAs.

Under the new law, penalties for missing or underestimating RMDs will be reduced. Failure to take the proper RMD from a retirement plan used to include a penalty of 50% of the shortfall. Beginning this year, the penalty is reduced to 25% or to 10% (if the individual corrects the issue within two years).

- Catch-up contributions will increase in 2025 for 401(k), 403(b), governmental plans, and IRA account holders.

Beginning January 1, 2025, individuals ages 60 through 63 years old will be able to make catch-up contributions up to $10,000 annually to a workplace plan, and that amount will be indexed to inflation. (The catch-up amount for people age 50 and older in 2023 is currently $7,500.) If you earn more than $145,000 in the prior calendar year, all catch-up contributions at age 50 or older will need to be made to a Roth account in after-tax dollars. Individuals earning $145,000 or less, adjusted for inflation going forward, will be exempt from the Roth requirement.

- Individuals can roll up to $35,000 from a 529 account to a Roth IRA in the name of the student beneficiary. The 529 account must have been in existence for at least 15 years. That provision becomes effective in 2024.

After 15 years, 529 plan assets can be rolled over to a Roth IRA for the beneficiary, subject to annual Roth contribution limits and an aggregate lifetime limit of $35,000. Rollovers cannot exceed the aggregate before the 5-year period ending on the date of the distribution. The rollover is treated as a contribution towards the annual Roth IRA contribution limit.

- Qualified Charitable Distributions

The new law also makes two notable changes to the Qualified Charitable Distribution (QCD) rules. The provision allows for individuals over 70 ½ to make a one-time election of up to $50,000 for a charitable distribution to a charitable remainder annuity trust, charitable remainder unitrust or a charitable gift annuity. And, beginning in 2024, the overall QCD limit of $100,000 will be indexed to inflation so that it will likely increase a modest amount each year.

Other notable provisions include:

- The creation of a “retirement savings lost and found” national database to help individuals find their benefits if they changed jobs, or if the company they worked for moved, changed its name or merged with a different company.

- Individuals can withdraw up to $22,000 from an employer-sponsored plan or an IRA for federally declared disasters.

- Beginning in 2024, employers have the option to match student loan payments with a contribution to the employee’s retirement plan account. The goal is to help workers who are burdened by student loans and cannot afford to make a contribution to their retirement plan by ensuring that they are accumulating some retirement savings even as they pay down their loan.

- Employers will also have the option to allow employees to create “rainy-day funds” in their retirement plan. Individuals would then be able withdraw up to $1,000 from the plan penalty-free for emergencies. The provision addresses a concern that spiked during the pandemic, when employers saw a big increase in the number of employees who were tapping their retirement accounts to cover unexpected expenses.

- Long-term part-time workers will become eligible for their company’s retirement plan after two consecutive years with at least 500 hours of service. Previous law required three years of service.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Capital Management, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

A new retirement bill known as the SECURE Act 2.0 is making its way through Congress. It aims to build on the SECURE Act of 2019 by giving Americans more incentives to save for retirement and proposes changes to required minimum distribution rules to allow individuals to keep their money in retirement accounts longer.

The SECURE Act of 2019 changed the rules around how an individual can save and withdraw money from retirement accounts. It was the first major legislative change to retirement tax laws in more than a decade. Now, new legislation under consideration includes extending required minimum distributions (RMDs) to later ages and increasing catch-up contribution amounts.

As a reminder, the original SECURE Act passed in 2019 included the following:

- Raised the age of required minimum distributions from 70 ½ to 72.

- Removed the ability to “stretch out” distributions from an inherited IRA over a lifetime for non-spouse beneficiaries.

- Allows 529 college savings plans distributions to pay back student loans.

- Penalty-free withdrawals of up to $5,000 from workplace savings plans to help offset the costs of having or adopting a baby.

The following provisions have been proposed and are under consideration, but none have yet been enacted into law under the SECURE Act 2.0:

- Delays RMDs until age 73 in 2022. Distribution requirements would shift to age 74 in 2029 and 75 in 2032, but there are variations of this timeline in other proposals.

- Raises the annual “catch-up” contribution amount to $10,000 for 401(k), 403(b) and 457(b) plans and to $5,000 for SIMPLE IRA or SIMPLE 401(k) plans. The exact age for the higher catch-up amount is under negotiation.

- Employers would be allowed to make matching retirement plan contributions to Roth 401(k) plans.

- Employers would be required to automatically enroll employees in 401(k) and 403(b) plans. Automatic deferrals would start at 3% to 6% of compensation.

- Employers would be allowed to make contributions to retirement plans for employees who are repaying student loans and not participating in a retirement savings plan.

The SECURE Act 2.0 was passed by the House of Representatives in March with a 414 to 5 vote. A separate bill called the EARN Act was introduced in the Senate in September. Both bills would make significant changes to RMDs, but there are differences in the two bills’ RMD provisions. The odds of passing a major retirement bill before the end of the year look promising, but nothing is expected to get done until after the midterm elections in November.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Capital Management, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

In response to the increasing number of financial fraud cases against seniors, regulators have implemented new rules to protect older clients. SEC and FINRA rules require financial advisors to ask their clients if they would like to designate a person to be contacted in the event that the advisor suspects fraud or mental decline.

What is a “trusted contact person?”

A trusted contact is someone who Nelson Roberts Investment Advisors can get in touch with to:

A trusted contact is someone who Nelson Roberts Investment Advisors can get in touch with to:

• Address possible or suspected financial exploitation involving your account;

• Confirm your contact information in case we have trouble reaching you;

• Confirm if there is someone acting as a legal guardian, an executor, a trustee, or holder of a power of attorney; or

• Determine your mental or physical health status.

It is important to note that your trusted contact does not have authority to access your account or make transactions on your behalf. Instead, the trusted contact’s role is to help us contact you; to provide the identity of any legal guardian, executor, trustee, or holder of a power of attorney; or to help us guard against financial exploitation.

Why should I add a trusted contact person to my account? Investment advisors often serve as the first line of defense when it comes to cases of possible financial exploitation. A trusted contact person is another resource to help protect you and your loved ones against financial abuse. A trusted contact person is another way of protecting your personal assets when something unexpected happens in your life. It adds an additional level of security to your account.

Who can be a trusted contact?

Trusted contacts are usually family members or close friends— people you trust and who are likely to be in the best position to know your current situation. A trusted contact must be at least eighteen years old. Please note, a trusted contact person need not be the same as someone who acts as a representative under a power of attorney.

Part of your financial planning should include identifying people who Nelson Roberts Investment Advisors can contact if we suspect you are a target of financial exploitation or if we see signs suggesting that you are becoming unable to manage your finances alone. Please contact us if you wish to add a trusted contact person to your account.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Roberts Investment Advisors, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.