Nelson Capital Management

The “Shake it Off” Market

Asset Management, Companies and Industries, Investment Themes, The Economy

January 3, 2024

The “Shake it Off” Market

2023 presented shocks galore, and with every ordeal, the equity market seemed to take Taylor Swift’s lyrical advice: “shake it off.” Geopolitical conflict, debt ceiling brinksmanship, a (still) possible government shutdown, student loan payments restarting, a troubled commercial real estate market, record and rising national debt—nothing seems to bother the market. Even the March bank failures were shrugged off completely. The S&P 500 finished the year up 26%, boosted by a torrid late year 16% rally that began around October 26.

Most of the equity market’s performance has been driven by the “Magnificent 7” (Apple, Amazon, Alphabet, Meta, Microsoft, Tesla, and Nvidia), which have been buoyed by developments in artificial intelligence. These seven stocks rose a combined average of about 75% in 2023, while the remaining 493 companies in the S&P 500 were up only ~11.5%. Since the Magnificent 7 make up about 30% of the index, their outsized returns helped power the index to near record highs.

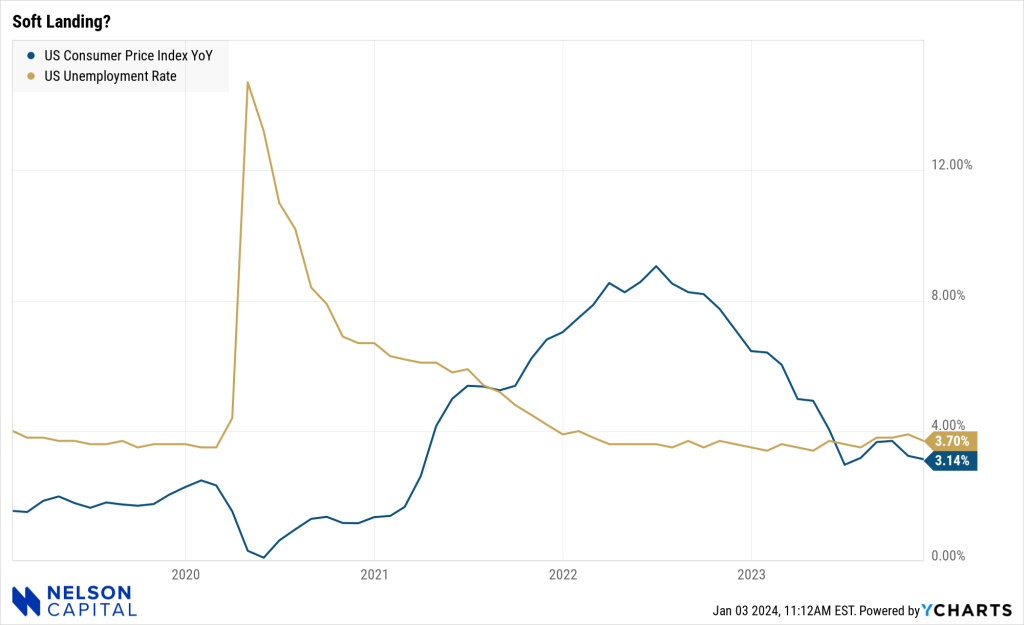

How is the market managing to stay resilient? Setting aside enthusiasm for AI, many now believe that the US economy is headed for a “soft landing” scenario, in which the Federal Reserve brings inflation down to its 2% target without causing a recession. In fact, this is now the consensus view among economists. About 70% of business economists polled in the National Association for Business Economics (NABE) August of 2023 survey said that a soft landing was at least “somewhat likely.” Only five months prior, the same NABE survey indicated that only 30% of economists believed a soft landing was possible.

Those who believe we are heading for a soft landing might be satisfied with the low unemployment number and recent inflation trend, but we are unable to “shake off” these other concerns

The latest batch of data has indeed signaled that inflation is continuing to move lower toward the Fed’s target. Moreover, we have not yet seen a significant slowdown in the economy or the labor market. Unemployment remains below 4% and job growth has been solid. Consumers are spending at a healthy clip, particularly on experiences and events like Taylor Swift concert tickets. At its latest meeting, Fed Chairman Jerome Powell noted that “inflation has eased without a significant increase in unemployment.” The Fed is forecasting that it will be able to make three cuts to its benchmark target rate this year, although market participants are (perhaps too optimistically) pricing in six rate cuts. For many companies and consumers, these cuts will be a welcome reprieve from higher borrowing costs. Analysts are meanwhile forecasting double-digit earnings growth for S&P companies in 2024.

Everything looks rosy. So is it time to pop the champagne and celebrate the soft landing along with everyone else? Maybe not yet. We are reminded of Warren Buffett’s wisdom to “be fearful when others are greedy.” The final push to lower inflation from its current 3.1% level to the Fed’s 2% target may be the toughest yet. If there is an unexpected jump in inflation, the Fed may pivot back to rate hikes, or else pivot back to keeping rates “higher for longer.” Of any fear, we are most focused on the potentially lagged effects of the Fed’s monetary tightening campaign. We have not yet seen a recession, but it could just take longer than most people expect for the rate hikes to negatively impact the economy.

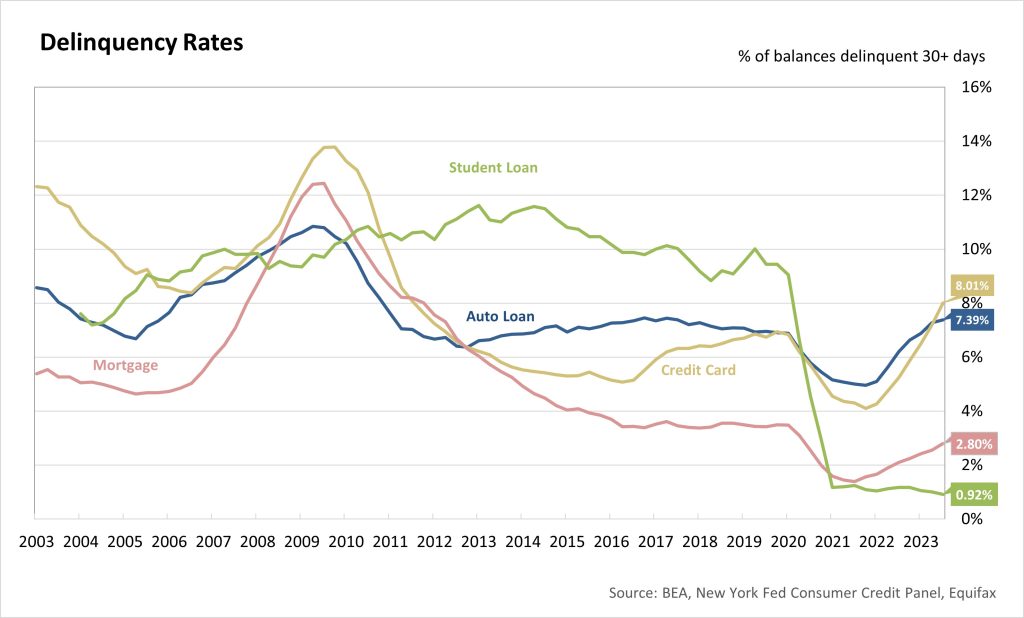

Furthermore, we still have concerns about the headwinds facing consumers, which we outlined last quarter. A paper by the SF Fed published in August hypothesized that excess savings built up during the pandemic would be fully depleted around the third quarter of 2023. The SF Fed in November published a revision to that paper based on new data that expanded estimated excess savings, indicating that households actually held about $430 billion in the third quarter of 2023. Be that as it may, these savings cannot last forever. We have also seen delinquency rates notch 10-year highs for both credit card and auto loan payments. Student loan repayments only recently restarted, which presents another headwind for all who carry student loans.

Those who believe we are heading for a soft landing might be satisfied with the low unemployment number and recent inflation trend, but we are unable to “shake off” these other concerns. We still see opportunities in the equity market, but we prefer attractively valued companies that could withstand a potential recession. We have also been active in the bond market, and we recently extended duration in client portfolios. There is also more than $6 trillion sitting in money market funds earning about 5% yields. These earnings could provide a tailwind if interest rates move lower and these funds are deployed into the equity and bond markets.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Capital Management, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

Receive our next post in your inbox.