Nelson Capital Management

What Could Go Wrong?

Investment Themes, Quarterly Commentary, The Economy, Wealth Management

April 1, 2024

What Could Go Wrong?

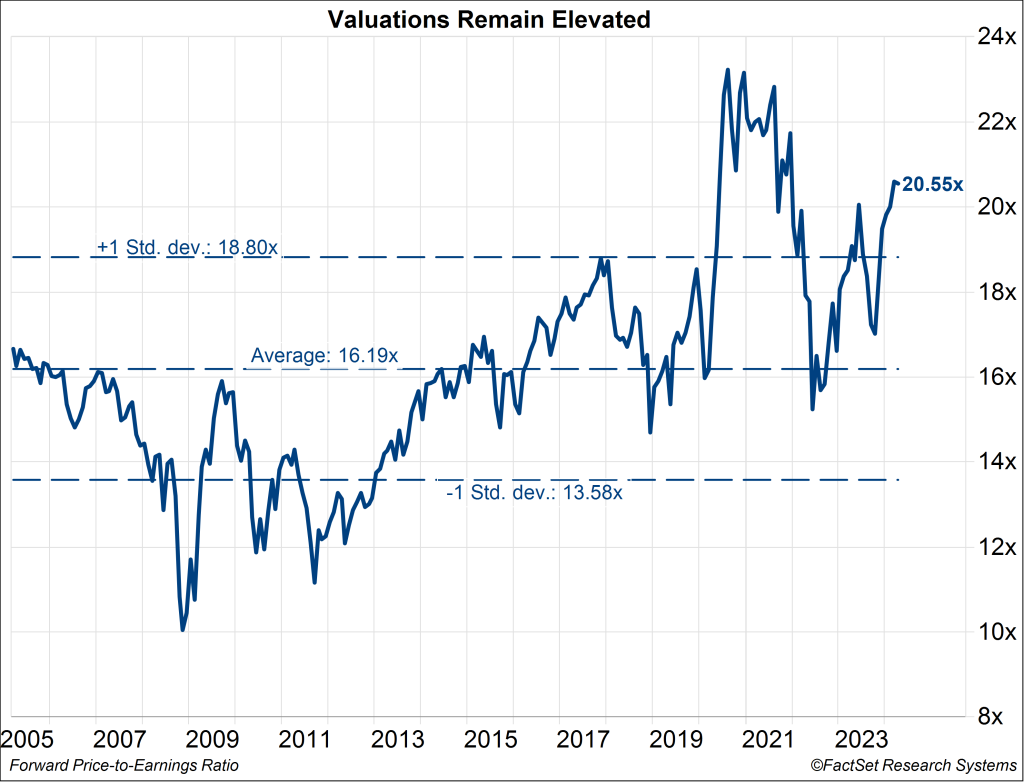

After shaking off the worries of 2023, equity markets started off 2024 with a bang. The S&P 500 rose 10.5% in the first three months of the year, driven by growing hopes that the US economy is on track to achieve a soft landing. The forward price-to-earnings ratio of the S&P 500 sits at around 21.7x, about 30% higher than the 25-year average of about 16.6x. Artificial intelligence enthusiasm helped boost returns, driving several of the largest technology leaders such as Meta (tkr: META) and Nvidia (tkr: NVDA) to new record highs. The “Magnificent Seven” from 2023 (Apple, Amazon, Alphabet, Tesla, Meta, Nvidia, and Microsoft) has seen divergence within the group this year, as Tesla (tkr: TSLA) and Apple (tkr: AAPL) have lagged their more AI-focused peers, down about 30% and 11%, respectively. Crypto excitement is back, with the price of Bitcoin up over 60% in the first quarter of the year, boosted in part by the SEC’s approval of exchange-traded funds that track the price of Bitcoin. Some of the unprofitable companies that struggled as interest rates began to rise in 2022 have seen a resurgence this year—for example Carvana (tkr: CVNA), which is up over 60%. Consumer sentiment has rebounded from the depths of 2022, and consumer spending remains healthy despite worries that excess savings are dwindling.

After shaking off the worries of 2023, equity markets started off 2024 with a bang. The S&P 500 rose 10.5% in the first three months of the year, driven by growing hopes that the US economy is on track to achieve a soft landing. The forward price-to-earnings ratio of the S&P 500 sits at around 21.7x, about 30% higher than the 25-year average of about 16.6x. Artificial intelligence enthusiasm helped boost returns, driving several of the largest technology leaders such as Meta (tkr: META) and Nvidia (tkr: NVDA) to new record highs. The “Magnificent Seven” from 2023 (Apple, Amazon, Alphabet, Tesla, Meta, Nvidia, and Microsoft) has seen divergence within the group this year, as Tesla (tkr: TSLA) and Apple (tkr: AAPL) have lagged their more AI-focused peers, down about 30% and 11%, respectively. Crypto excitement is back, with the price of Bitcoin up over 60% in the first quarter of the year, boosted in part by the SEC’s approval of exchange-traded funds that track the price of Bitcoin. Some of the unprofitable companies that struggled as interest rates began to rise in 2022 have seen a resurgence this year—for example Carvana (tkr: CVNA), which is up over 60%. Consumer sentiment has rebounded from the depths of 2022, and consumer spending remains healthy despite worries that excess savings are dwindling.

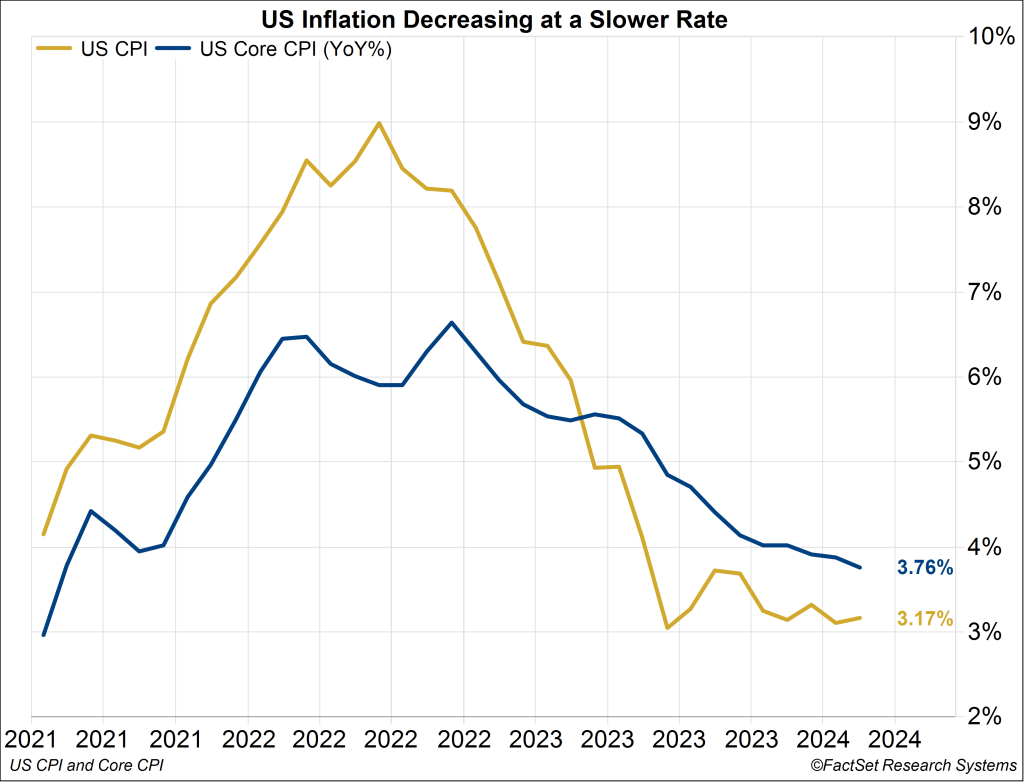

Many are confident that the Federal Reserve is on track to achieve its monumental task of bringing inflation lower without causing an economic recession. There are reasons to believe the narrative that the US is headed for a soft landing. Inflation has generally trended lower, without denting the strong labor market. Headline inflation has stalled out at just over 3% since last summer, but core inflation, which strips out the volatile food and energy categories, has trended gradually lower and currently sits at about 3.75%. Everyone seems convinced that inflation is heading toward the Fed’s stated target of 2%, which will allow the Fed’s monetary tightening cycle to end soon. At its March meeting, the Fed held rates steady at 5.25%, but maintained its forecast that its benchmark target rate would be cut three times in 2024. This helped assuage investor concerns that the central bank might keep rates “higher for longer,” which could eventually begin to adversely impact households, small businesses, and the broader economy.

However, some inflation metrics, particularly services inflation, remain stubbornly high. In fact, the two most recent inflation reports were hotter than expectations. Investors and the Fed seem to be taking a “glass half full” view, brushing off these two hotter reports as aberrations in an otherwise sustainable downward trend in inflation. In addition to maintaining its outlook for three rate cuts to its benchmark target rate this year, the Fed also hinted at a near-term slowdown in the pace of its Quantitative Tightening (QT) campaign. The Fed has been reducing the size of its balance sheet by an average of $62 billion per month, bringing the total balance sheet assets from a peak of $9 trillion in April of 2022 to a current level of $7.5 trillion. So far, we have not seen any major liquidity disruptions.

The more concerning question that no one seems to be asking is: What if inflation reignites and moves higher from here? Could the Fed be pressured to increase rates from current levels?

While we are optimistic that the US economy will achieve a soft landing, we are also looking for what could possibly go wrong. We want to ask the questions that no one seems to be thinking about. What if inflation remains stuck at over 3%? This could drive the Fed to keep rates where they are, scrapping the planned rate cuts later this year. In fact, Atlanta Fed President Raphael Bostic recently reiterated his more hawkish view that there should only be one rate cut for the remainder of the year. The more concerning question that no one seems to be asking is: What if inflation reignites and moves higher from here? Could the Fed be pressured to increase rates from current levels? While we do not believe this to be the base case scenario, we think it is a scenario worth at least considering. As most brokerage accounts and crypto wallets have seen substantial gains over the past 18 months, consumers may start thinking that it is a great time now to remodel the kitchen, take that expensive trip, or purchase that new car they have been eyeing. This behavior in aggregate could push inflation higher, forcing the Fed to reevaluate its plan to cut rates, or even compelling the Fed to hike rates. If this occurs, it would call into question the current high valuation of the equity market, which has all but assumed the US will glide into a soft landing.

Fortunately, the bond market still offers an attractive, low risk alternative to the equity market, generating yields of 4.5-5%. Despite some evidence of froth, many companies have churned out solid earnings, helping support current valuations. The election and current geopolitical turbulence could create volatility this year, but these events have not been the focus for investors. We continue to watch for contrarian signs that inflation might not be on a glidepath towards 2%. We are prepared to further reallocate to fixed income to reduce risk if we begin to see inflation reignite.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Capital Management, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

Receive our next post in your inbox.