Nelson Capital Management

The Run on Private Credit

Asset Management, Companies and Industries, Investment Themes, The Economy, Wealth Management

June 10, 2026

The Run on Private Credit

Investors are actively trying to pull massive amounts of money from private credit funds including one of the largest, Blackstone’s Private Credit Fund (BCRED). In the second quarter of 2026, investors asked to redeem 10% of the fund’s shares, up from about 8% in the first quarter. That amounted to a cash-out demand of $4.4 billion.

In response, Blackstone lowered its redemption rate. The firm announced it will limit redemptions from the $79 billion fund to a 5% quarterly cap. This is a reversal from its strategy in March, when management opted to pay out the full amount requested.

In response, Blackstone lowered its redemption rate. The firm announced it will limit redemptions from the $79 billion fund to a 5% quarterly cap. This is a reversal from its strategy in March, when management opted to pay out the full amount requested.

This abrupt about-face highlights a rising, systemic financial strain on managers of large private credit funds. These vehicles were aggressively marketed to individual retail investors who are now asking for their money back.

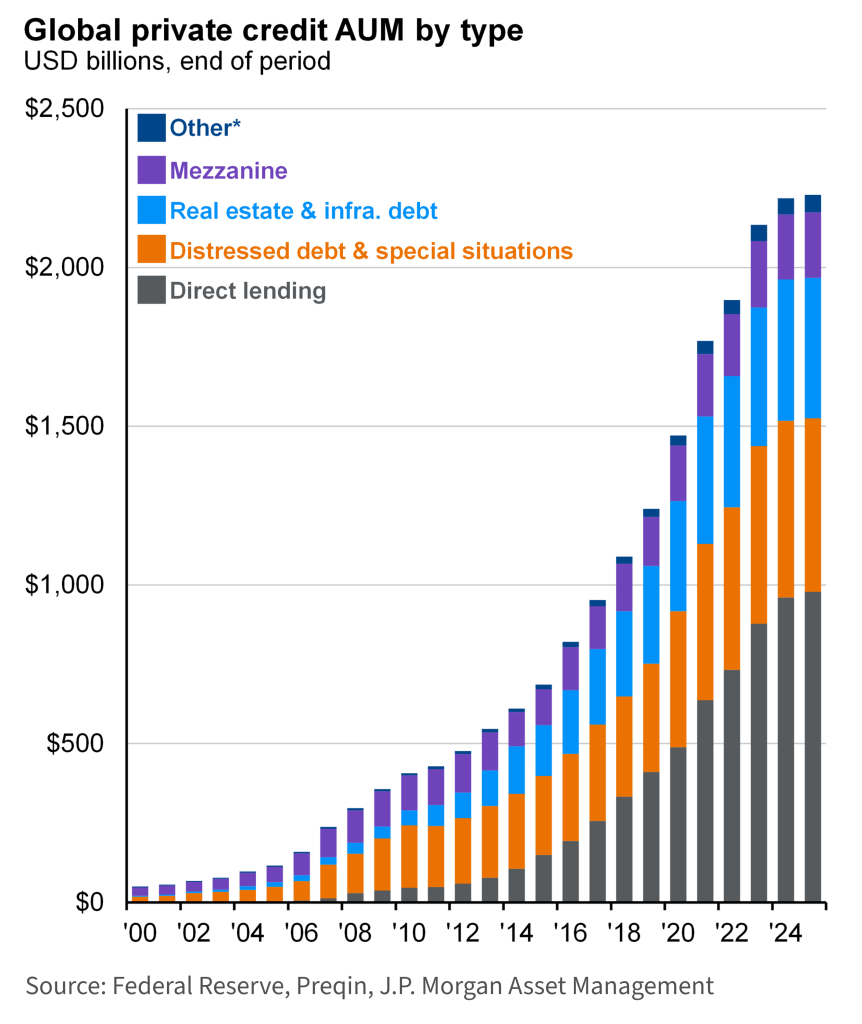

The Evolution of Non-Bank Lending

To understand how we arrived at this point it’s important to understand where private credit originated from.

- The GE Capital Era (1980s–1990s): Long before private funds took over, captive corporate finance arms like GE Capital were the kings of private credit. They financed railcars, commercial aircraft engines, and MRI machines. This era trained a massive generation of lenders who eventually splintered off into the broader financial ecosystem.

- The 2008-2009 Financial Crisis: The catalyst for private credit growth was the post-crisis bank regulation. To protect the global banking system, regulators cracked down on traditional commercial banks, effectively barring them from lending to companies with highly leveraged profiles

- Zero Interest Rates (2008-2015 and 2020-2022): The corporate demand for debt didn’t vanish just because banks were restricted. Simultaneously, institutional investors who were starved for yield during periods of Zero Interest Rate Policies (ZIRP), flooded into alternative asset spaces, eager to capture a premium by locking up cash in private loans.

Eventually, the institutional well ran dry. To keep growing, private credit asset managers needed a new source of capital. They found it in the retail wealth channel.

Retail Investor Inflows

The institutional private credit model is built on a drawdown structure. Institutional investors commit money, and managers only call that capital when they find a good deal. The cash doesn’t sit around diluting performance.

But to sustain explosive asset growth, mega-managers like Blackstone, KKR, Apollo, Blue Owl, and Ares aggressively expanded into the retail and private wealth channels via interval funds and non-traded Business Development Companies (BDCs) like BCRED. This changed the game entirely by introducing a continuous subscription model.

When a retail investor buys into a fund, that cash hits the balance sheet immediately. If it sits idle, it drags down the fund’s Net Asset Value (NAV) and dividend yield. Consequently, retail private credit managers are under pressure to deploy capital fast.

This pressure triggered a hyper-competitive race to win deals. To invest incoming cash during the peak of the boom, managers were forced to accept weaker loan covenants, lower pricing, and higher leverage.

Now, the music has stopped. Investors piled into these funds because they invest in high-interest loans to midsize companies and distribute most of the income via juicy dividends. But the retail sentiment turned fiercely bearish this year over increasing loan defaults and the potential for future losses and particularly from aggressive lending to the software sector.

The Asset Degradation Loop

To attract retail wealth these funds promised periodic liquidity. But because you can’t easily liquidate a five-year corporate loan, funds built in liquidity gates, capping quarterly redemptions at 5% of total assets.

While these gates protect the fund from a catastrophic, overnight bank run, they trigger a slow-motion disaster for the quality of the remaining asset pool:

- Forced Liquidation of Prime Assets: If a fund hits its gates during a period of market panic and new inflows dry up, the manager must source liquidity somewhere to meet that 5% redemption demand.

- Selling the Best, Keeping the Worst: A manager looking for quick cash will always sell or refinance their highest-quality, most liquid, and cleanest loans first.

- The Stressed Residual Pool: As a result, the non-redeeming investors who stay in the fund are left holding an asset pool that is increasingly leveraged and backed by worst-in-class, highly illiquid, or stressed corporate debt.

Blackstone isn’t alone. Redemptions across the industry soared in the first quarter, forcing firms like BlackRock, Blue Owl, and Ares Management to impose similar limits. Withdrawal requests have ranged from BCRED’s 10% to a massive 22% redemption request that Blue Owl faced for its flagship fund. This wave of announcements has knocked down the share prices of publicly traded alternative asset managers across the board.

The SaaS Tech Risk

Nowhere is this aggressive underwriting more obvious than in the technology sector. Historically, debt and high-tech didn’t mix because tech companies lacked physical collateral like factories or real estate.

Modern private credit threw that playbook out the window. Lenders fell in love with the recurring revenues of Software-as-a-Service (SaaS) models. Private equity sponsors bought software companies at premium valuation using heavy debt loads financed entirely by private credit funds.

To keep these highly leveraged capital structures alive in a higher-interest-rate environment, lenders are increasingly relying on Payment-in-Kind (PIK) interest. PIK allows struggling corporate borrowers to defer paying cash interest by tacking it onto the principal balance of the loan. While this keeps the loan listed as “performing”, it hides cash-flow insolvency.

The ultimate danger here is terminal liquidation value. If an industrial company defaults, its factories and machinery retain physical value. If an over-leveraged software company goes bankrupt, or gets disrupted by rapid advancements in artificial intelligence, its obsolete code is worth zero.

But as the broader credit cycle turns, two major macroeconomic realities are emerging:

Because private credit and syndicated leveraged loans absorbed the riskiest, most heavily indebted borrowers over the last decade, the public high-yield bond market has actually become structurally safer. Double-B rated bonds now make up roughly 60% of the public high-yield index (up from 35% historically), while the riskiest Triple-C segment has shrunk to just 9%. The systemic risk has effectively been pushed out of the public eye and into private portfolios.

Corporate borrowers that executed leveraged buyouts (LBOs) in the easy-money days of 2020 or 2021 did so when benchmark interest rates were near zero. Because private credit loans are floating-rate instruments, the subsequent interest rate hikes have caused corporate borrowing costs to skyrocket, aggressively chewing through equity values.

Some Wall Street analysts project that default rates in private credit could spike as high as 15% in the coming cycle. As private credit has grown larger than the public junk bond market, it is now the funding engine for middle-market corporate America. If the asset class fractures under default stress and redemption freezes, it won’t just hit retail investors. It could also trigger a credit crunch for many mid-sized American businesses.

The era of non-mark-to-market accounting allowed private credit managers to print steady 10% yields with little volatility is ending. As the gates close at the largest private credit funds, we are about to find out who maintained disciplined underwriting standards and who was greedy.

Receive our next post in your inbox.